Construction forecasters get more pessimistic – the difference a year makes

It’s that time of year when we look at forecasts and wonder just how bad or good the future will be for the construction industry.

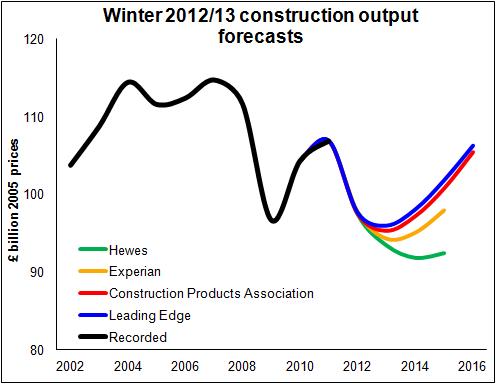

The top graph shows the latest prognostications and they look pretty miserable in the short term. The forecasters have nudged down their expectations, some lightly, some heavily, which means they now expect things to be worse than when they last forecast.

The overall picture they paint is of another year or possibly two of recession before the industry perks up a bit. But there is a spread in the views on how far the industry will fall before recovering.

The overall picture they paint is of another year or possibly two of recession before the industry perks up a bit. But there is a spread in the views on how far the industry will fall before recovering.

Interestingly the latest two forecasts to be produced, Hewes and Leading Edge, fall either side of those from Experian and the Construction Products Association, which we considered last month.

Much is made of this spread of opinion among forecasters. I’m occasionally asked who is most likely to be right or who has the best record. I see the reason for asking, but I’m worried it reveals a lack of understanding about forecasts and their purpose.

If we take as read that the forecasters know what they are doing, the spread of views adds business information rather than adding confusion.

Why? Because a wider spread of forecasts indicates greater uncertainty, something any strategic planner should note. It means increased risk. The differences simply reflect the different assumptions made about each element of uncertainty.

And any good forecast should give strong guidance on what the risks are, the scale of those risks and some clues as to the likelihood of the risks being realised or how much uncertainty surrounds it. The numbers and the central forecast can only tell you so much. The text and the analysis are important.

There is a philosophical point to be made here. Simply making a forecast changes the future. If, for instance, you are a business and forecast that you will go bust doing what you are doing then you end up changing what you are doing to try to avoid it.

I’m not sure how much notice the Government or policy makers take of construction forecasts, but you would hope that if the industry were heading for meltdown they might do something to avoid it.

The leap in output in 2010 is testament to the previous Government acting swiftly in bringing forward construction spending to stave off a worse recession. This is not something that the forecasters could realistically be expected to predict. But as we see in the graph, it made a huge difference to the shape of construction output.

For all that it can be instructive to compare what was forecast earlier with what happened and what is now forecast. You should be careful about drawing too many conclusions. Quite often poor forecasts prove right for the wrong reasons, while “better” forecasts can end up much wider of the mark. And as we all know if you make enough predictions you will always have one favourable one to point to.

For all that it can be instructive to compare what was forecast earlier with what happened and what is now forecast. You should be careful about drawing too many conclusions. Quite often poor forecasts prove right for the wrong reasons, while “better” forecasts can end up much wider of the mark. And as we all know if you make enough predictions you will always have one favourable one to point to.

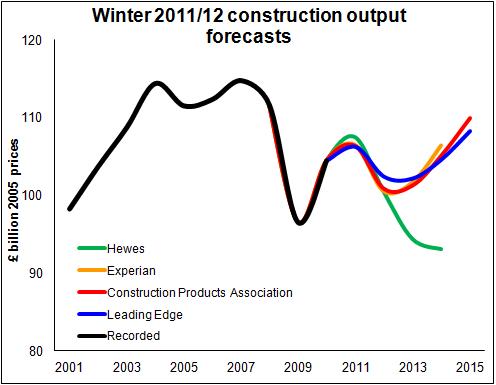

So let’s compare the latest construction forecasts with how the same forecasters saw things a year ago (see the second graph). The most obvious point of note is that 2012 turned out to be much worse than expected with about £3.5 billion less work than expected.

And looking at how the forecasters have revised their forecast further ahead we have to deduce that things look much less promising than they did in the minds of the forecasters a year ago. That is with the exception of the Hewes forecast which has been consistently bleaker from the outset.

Putting the Hewes forecast to one side, the average of the revisions for the other forecasts suggests about £8 billion less work this year and about £10 billion less in 2014 than was expected just a year ago.

So what we can say is that a year ago it helped your case to be among the more pessimistic forecasters if your aim was to match what the Office for National Statistics data suggest happened to construction.