Was it just the cold or is it a relapse?

There are plenty of people, “experts” indeed, who fully expect a double-dip recession for both the economy and, for that matter, house prices.

For them the data emerging for January’s performance appears to be, albeit gently, vindicating their position. They will no doubt seize with alacrity the retail figures from the British Retail Consortium showing the worst January sales data for 15 years.

Those who take a different perspective will write the slump in sales off to the coldest January in more than 20 years.

And it is in this context of confusion and conflicting views that the latest housing market survey from the surveyors’ body RICS is being assessed for signs of strength or fragility.

So what does the RICS survey show us? Well, in pretty much equal measure there was enough to remain happy about and enough to cause concern, depending on which end of the glass you take as your reference point.

The survey suggests that on balance house prices continued to grow pretty strongly, though mainly in the more affluent regions.

But the number of potential house buyers and seller walking through estate agents doors dropped dramatically.

The innately chirpy estate agents naturally see their glasses as half full, as the RICS assessment of the figures suggests.

“Surveyors are optimistic that these negative signs are a reflection of the extreme weather conditions experienced in the early part of the month. The number of surveyors expecting house prices to rise increased from 12 percent to 24 percent while the number of surveyors expecting sales to pick up over the next three months rose from seven percent to 24 percent in January,” says the note accompanying the survey.

But in a more cautious fashion, RICS spokesperson, Ian Perry goes on to say: “The cold snap in January clearly has a huge impact upon both supply and demand in the housing market with activity coming to a halt amidst the seasonal chaos. Activity and interest is likely to pick up in the coming months as the market experiences a spring bounce.

“House prices are likely to rise in the short term but if more supply continues to come onto the market, it is possible that the market will run out of steam in the latter part of the year.”

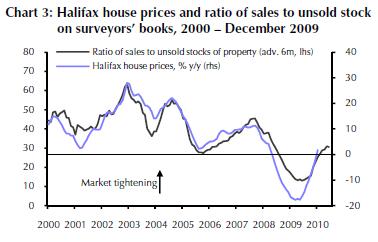

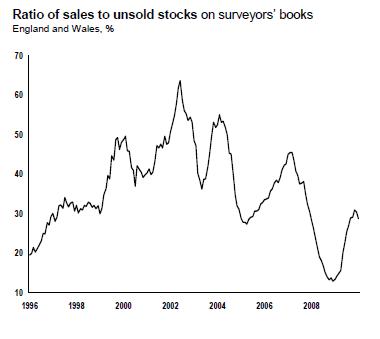

Possibly the most interesting measure recorded by the RICS is the sales-to-stock ratio. This does seem to be a pretty good forward indicator of price movement as can be seen by this graph (right) produced by the economics consultancy Capital Economics in its February UK housing market review.

Possibly the most interesting measure recorded by the RICS is the sales-to-stock ratio. This does seem to be a pretty good forward indicator of price movement as can be seen by this graph (right) produced by the economics consultancy Capital Economics in its February UK housing market review.

Roughly speaking the graph suggests that changes to the sales-to-stock ratio seem to track about six months ahead of price changes, as measured by Halifax.

The sales-to-stock ratio (the graph on the right is taken from RICS January Housing Market Survey) peaked this time around in November at 31, it drifted slightly south in December to 30.4 and rested in January on 28.8.

The sales-to-stock ratio (the graph on the right is taken from RICS January Housing Market Survey) peaked this time around in November at 31, it drifted slightly south in December to 30.4 and rested in January on 28.8.

The first question is: Is this the start of a decline in the ratio, or just a hyper-seasonal blip?

The second question is: If it is the start of a decline what does it mean for the direction of house price growth?

Time will tell, but what is evident from those busy trading residential property derivatives is that sentiment is certainly weakening.

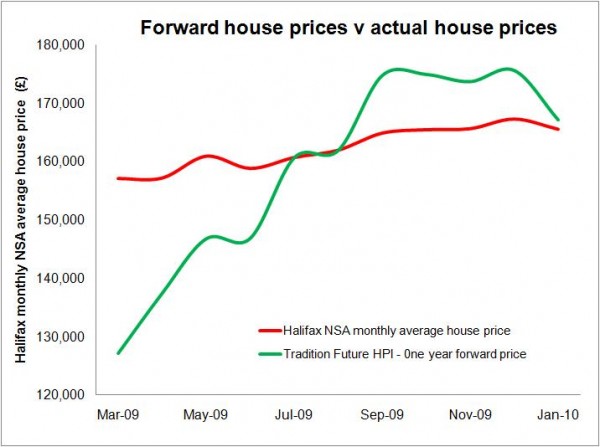

The graph below shows the growth in house prices, as measured by Halifax, and the one-year forward price, as measured by the Tradition Future HPI. Put simply the gap between the two represents the market view of the expected rise in house prices over the next 12 months.

In September the traders were punting on a 6% rise in prices, now that figure has narrowed to 1%.

In September the traders were punting on a 6% rise in prices, now that figure has narrowed to 1%.

Much of what will lie behind the changing sentiment is the growing worry that the house-price revival rests on a very narrow slice of the market – the low loan-to-value, equity-rich buyers in the south.

Added to this will be the knowledge that with low interest rates reluctant sellers are far fewer in the market than they might otherwise be, so supply is very much reduced, which in turn is (perhaps only temporarily) propping up prices.

There are also growing fears that the mortgage market will start to present yet more problems, as irritated savers choose to put their cash into anything but a building society or bank deposit accounts while lenders struggle to meet their obligation to find enough cash to fill the hole left by the wilted wholesale money market.

That is a £300 billion sized hole, according to the Council of Mortgage Lenders.

This suggests mortgage rates may rise regardless of any increase in the official Bank rate.

Following up on CML’s comments last week, Robert Peston of the BBC takes a particularly bleak view of this problem in his latest blog.

Meanwhile, the spectre of inflation still stalks – today’s weekly fuel prices report, for example, shows a further 1% month-on-month rise in petrol and diesel prices – adding ever greater likelihood to an earlier rather than later rise in interest rates.

Tomorrow’s Bank of England inflation report will be more thumbed than usual by journalists and analysts alike looking desperately for clues to the state of the economy and the possibility of a double dip.

One thought on “Was it just the cold or is it a relapse?”

Brian,

Very interesting analysis. Listening to the Today programme in the dark a couple of days ago was even more depressing than usual, with Roger Bootle and another economist going all Nostrodamus and predicting more economic pain.

Regardless of the numbers – which is far from my strength – my gut is telling me it may have to get worse before it gets better.

Comments are closed.