Brighter outlook from forecasters, but severe risks remain

The forecasts from Hewes & Associates and Leading Edge sit interestingly against the other winter forecasts for construction output released over the past couple of weeks.

They seem to back up the mood among other forecasters that construction workload might not fall as much was feared in the middle of last year.

They seem to back up the mood among other forecasters that construction workload might not fall as much was feared in the middle of last year.

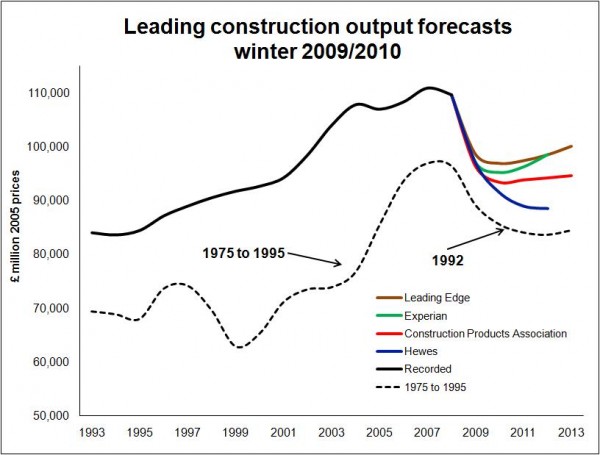

But what is most notable about the various forecasts when we put them together (see graph) is the spread of central projections for the path of construction output.

I suspect while there are differences of view, the extent of this spread of expected outcomes is more a reflection of the high degree of uncertainty.

The balance of risks inherent in those forecasts at the more optimistic end of the scale will tend to be on the downside, while Hewes will most likely have shaded risks more pessimistically.

Much of the uncertainty within these forecasts will be around just how fast the public sector cuts impact on construction output, both directly though capital spending cuts and indirectly through their effects on the wider economy.

It is fair to say that the broad expectation is for annual double-digit falls in non-residential public new work.

There are of course other risks, such as rising inflation sparking an earlier than expect interest rate rise. This could put severe downward pressure on both private housing and the commercial sector.

Despite this there is a slightly perkier view of the private house building sector and on balance the forecasters expect an earlier return to growth within the commercial sector.

Also the repair and maintenance sector does appear from the official figures to be holding up better than expected.

Given this more optimistic view of the volume of work expected by forecasters, it will be interesting to see whether firms become bolder and prices firm up a little after a destructive downward spiral in bid prices.

Put simply the cuts in prices associated with a recession tend to do more damage to the industry than the reductions in volumes of work.