Why we should be cautious about seeing the RICS survey as a signpost to growth in UK construction

The press release headline for today’s RICS construction market survey suggests the industry will turn the corner and grow in 2013. That sounds like encouraging news.

Sadly, it is probably over optimistic and probably overstates the results of the survey.

Sorry to burst one of the all too few happy bubbles you’ll see this year. But there’s a host of reasons to be cautious over the interpretation of the latest survey.

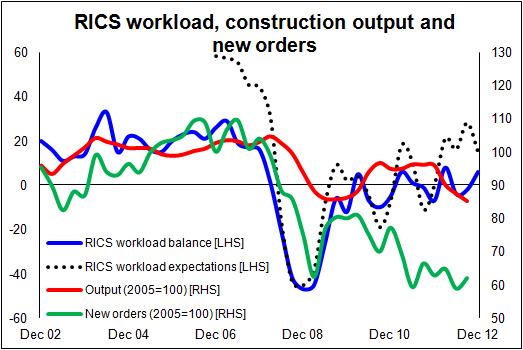

The RICS construction survey provides a useful indication of what lies ahead for those working on the ground, as the work of those surveyed tends to be weighted towards the early stages of construction. It adds positively to the array of construction data.

The RICS construction survey provides a useful indication of what lies ahead for those working on the ground, as the work of those surveyed tends to be weighted towards the early stages of construction. It adds positively to the array of construction data.

But like all surveys and forecasts it has limitations and its findings need close interpretation and consideration when there are structural changes within the industry.

Only by knowing what a number relates to can you infer meaning from it.

To get to the point, what initially surprised me when I read the press release was that it suggests growth in 2013, albeit slight. The consensus of forecasts and a wealth of other data point to a fall.

The graph above shows the RICS workload index and workload expectations index against the indexed values of construction output and new orders. Now they are not measuring the same things (RICS is measuring balances of up and down, while the ONS is measuring volume). But on gut feel alone I would be more surprised if the industry grows than if it shrinks in 2013 based on the official data.

Not that I know which way the industry will go next year.

The graph also shows that the balance of optimists against pessimists among the surveyors surveyed has been pretty positive for some while.

That said the RICS’s calculation of the growth in workload expected by the survey respondents is small, between flat and 2.5%. And it must be noted that this range reflects the fineness of the scale used for assessing expectations of future workloads rather than a judgment on the range of expectations.

So what the survey is saying is that the respondents on average expect the smallest amount of positive growth and on balance many more firms expect to do better than worse.

But given the way the question is framed we don’t really know whether they are reading growth in nominal (cash) or real terms (adjusting for inflation). If they are not taking into account inflation the survey may be saying slightly nominal growth, but probably a real-terms decline, assuming inflation at 2.5%.

To my knowledge the survey does not weight respondents according to their size. This is not necessarily a major fault given the purpose of the survey, but it means that there is greater uncertainty over actual volumes in the results.

There are other technical issues that need to be accounted for. The question asks how firms expect to be doing.

It’s well known that in normal circumstances if you ask someone how they expect to do they will tend towards being positive. This optimism bias may well be boosting the figures. If we look to the Markit/CIPS construction survey, its expectation results are wildly optimistic when judged against what actually happened.

In fairness in times of huge stress respondents can get carried away and overstate the negatives leading to a pessimism bias.

And if we want to get more technical we should also take account of the possibility of survivor bias. Firms that have just gone bust don’t fill in the forms, so the sample is skewed towards better performing firms.

But there is an important point to be taken into account that relates to changes in the real world, rather than the fraught problems of surveying businesses views. In October I thought to question the optimism I found then in the RICS construction survey.

I suggested that the survey have been influenced by surveying firms doing increasing amounts of overseas work in the UK.

The Office for National Statistics figures for turnover among architectural and engineering services show a near 9% rise in nominal terms in turnover, albeit a crude measure, over the past year. This follows a period of relatively strong growth.

Interestingly too, when we look to the ONS Pink Book, as I did in a recent blog, we see that there is a growing positive trade balance in the value of services traded.

This suggests UK-based surveying businesses are filling their order books ever more with work being done abroad. That’s brilliant and should be applauded.

The danger for this survey is that when asked “how’s business look in the year ahead?” they are talking about business in general as much if not more than business in the UK.

So naturally they will be more optimistic than the UK construction market would lead them to be.

For all these reasons I would be very cautious about concluding from the RICS construction survey that the industry has turned a corner, especially if you think the corner heads upward.