The latest construction forecasts may be more optimistic, but the risks haven’t gone away

For those who like their news good, the story in the latest construction industry forecasts is that the mood is less pessimistic than it was three months ago.

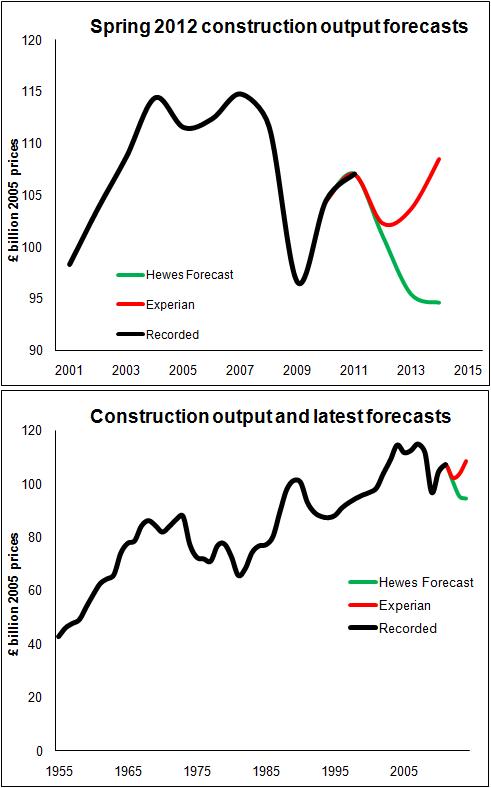

The two forecasts out so far in this spring round – Experian and Hewes & Associates – both tweaked their figures upwards for output over the next three years.

Looking at this year, Experian revised its forecast from -5.6% to -4.4%, while Hewes saw a case to reduce the fall from -6.5% to -5.6%. Both also revised their figures upward for 2013 and 2014.

That suggests that 2012 is still set for a hefty drop, but not as big as was thought at the start of the year.

The top graph shows the basic shape of forecasts for construction output over the next three years. The bottom graph puts it all in a wider historic context.

The top graph shows the basic shape of forecasts for construction output over the next three years. The bottom graph puts it all in a wider historic context.

The increased optimism should come as no surprise. There’s been slightly better-than-expected data released of late and the Euro area did manage in the intervening period to tie a bandage around the weeping economic sore that is Greece.

Clearly the two forecasts represent a very different view of the future. This in part reflects the huge risks that remain in the economy that could impact greatly on construction.

Hewes chooses to take a dimmer view of these risks. If you like, more of the risks are taken into account in the assessments of likely outcomes. This leads to the view that construction will remain in recession throughout the forecast period.

In contrast, the Experian forecast makes the explicit assumption that the Eurozone will muddle through and it acknowledges the downside risks that household demand could be much weaker and oil prices could create inflation problems.

So while the Experian’s forecast represents its view of what is most likely to happen, there are big risks on the downside. And while the forecast is a shade more optimistic than in the winter Experian didn’t change its view on the shape of growth in most sectors.

There was a technical tweak to housing starts within the forecast, but broadly its outlook for housing is the same.

But the most marked changed was on the prospects for non-housing repair and maintenance work. Experian now sees growth where a few months ago it feared there may be a decline.

There are various factors that have convinced Experian to alter its view, notably evidence that the public sector appears to be spending to save. So, for instance, more energy saving work is being done.

Comparing the two forecasts throws up what is really interesting about the prospects for construction in the coming years. Hewes and Experian clearly have very different expectations of what is most likely to happen.

But when you look in detail much of what is in the two forecasts is similar.

The difference is that where Experian sees private sector growth coming with modest or strong performances from four big sectors – private new housing, commercial building, infrastructure and non-housing repair and maintenance – Hewes sees continued recession.

This divergence of view highlights the huge uncertainty over how much appetite the private sector has to boost construction output.

So, while on private housing there is little doubt that the Government has given house builders huge support, there remains a question over whether this will drive growth in profit more than in production.

The prospects for infrastructure do seems relatively rosy, but there is always the lingering threat that a rise in economic uncertainty could lead to the cancelling, shrinking or slowing down of capital projects.

Now, no one is expecting great things from the commercial sector in the near term. Experian expects a 3% fall followed by a 3% rise in 2013 before a healthy rise of 6% in 2014. Hewes sees three years of decline, not a huge decline but significant.

However, there is concern that lately much of the support for work in the sector has come from offices and retail projects and a large slice of this coming as mothballed schemes were restarted. This will have helped to put a floor under the sector and created some growth last year. Looking to the future the big questions is what will drive growth outside of the hot spot that is London.

Turning to private non-residential work, there’s a strong case to support Experian’s expectation of growth. The green agenda, for instance, has taken root and does offer much opportunity for the construction sector. But against this must be weighed against the short-term pragmatism of businesses who find themselves strapped for cash. It is likely that the strength of the economy will play its part in determining which way this sector goes.

But for all the detailed assessments of each sector and the respective cases for and against growth, the lingering doubt I am left with is how the low levels of orders won by contractors, according to the official figures, will translate into real work on the ground (construction output).

The relationship between orders and output is far more complicated than one might initially suspect. I’ll not go into detail here, except to highlight one point.

In the run up to the recession there was a surge in large projects won by contractors. This was partly why some of the larger firms were so slow to accept that the industry was heading for recession.

Many of these big contracts will have run for many years, propping up output through the recession. But most of those that are still running will be coming to an end soon.

That leaves a big question in my mind over what will fill the gaps they leave?