Latest construction output figures support recession fears

The latest construction output figures add further weight to fears that the industry is heading into recession.

At first glance the figures may seem reasonably positive. The volume of work carried out in the three months to January was a shade (0.7%) up on last year.

This seems to suggest that construction is holding its own in tough circumstances.

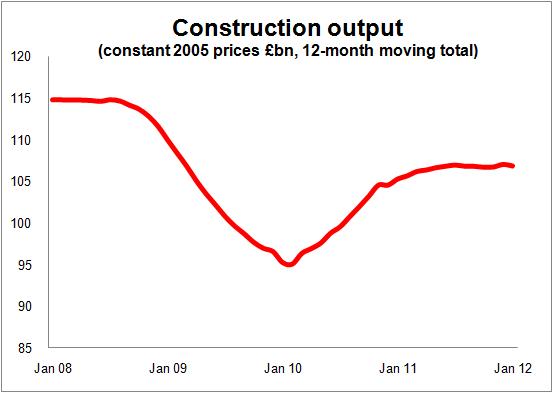

Looked at on an annualised basis construction has been broadly flat since May last year, as we can see from the graph.

Looked at on an annualised basis construction has been broadly flat since May last year, as we can see from the graph.

But if we pull the data apart the picture is far less reassuring.

The first thing to note is that we have just had one of the milder winters, so we would have expected a lift in output and for the figures for the winter months to reflect that. So it’s probably worth shading down the latest figures to get a fairer comparison of how construction is performing.

The exact impact of this is hard to quantify, but it is worth bearing in mind.

The reality is that reading the official output figures on a monthly basis has become more of an art than an imprecise science.

The next point to make is that the performance of the construction industry overall is increasingly dependent on the performance of the private sector, as public spending shrinks.

The public sector has so far held up better than many expected. If we look just at public sector new build, ignoring infrastructure, we see that output is still more than 50% above the level when the recession hit. That amounts to about £6 billion more spent a year in 2005 prices.

Meanwhile, the private sector equivalent is down more than a quarter from the peak. That represents an annual £16 billion drop.

The string has been taken out of this drop not just by the £6 billion extra spend on new buildings by the public sector, but also by an annual increase of about £6 billion in infrastructure output.

What we would hope to see in the coming couple of years is a rebalancing with the larger private sector coming up reasonably strongly as the public new building spend falls fairly fast and growth in infrastructure work eases.

But while we have seen a bounce in private sector new build, up about £5 billion from the depths of the recession, the pace of growth has waned recently.

Much of this bounce back in output in the private sector will have been due to restocking effects. The danger is that this effect can be misread as underlying growth and lead to over optimism.

The effect is particularly relevant to private house building. Here we saw work on numerous sites halted and new starts plunge as builders sought to sell off existing stock.

However as demand settled, the pipeline of work needed to be re-established. This will have boosted output for a short period as firms not only built out existing work, but also looked to backfill their production pipeline.

So it should be no surprise that the level of work is now starting to flatline after an initial surge.

What is more concerning is that the data for orders being won by construction firms adds little hope that we will see the amount of underlying growth in private sector construction needed to off-set the inevitable fall in public sector work.

This is in large part why the forecasters expect construction to experience a recession this year. The question now seems less: Will we avoid it? But more: How deep will it be?