Latest construction data underline tough challenge for the industry in 2012

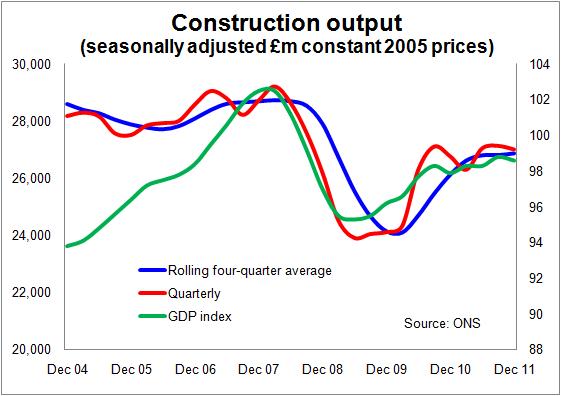

The latest official statistics show construction output fell by 0.5% in the final quarter of last year. That is in line with the statisticians’ estimate put out with last month’s GDP data.

This fall fits with the raft of other industry data that has shown construction work falling.

And it also fits with industry forecasts that construction is set to dive into recession again for the best part a couple of years.

There are other surveys, the Markit/CIPS survey for example, that paint a slightly rosier picture. But if we mentally adjust that for its normally jolly view of the world, it too points to and industry far from buoyant.

There will be revisions to the final quarter figure. The estimated deflators applied to the latest current price data will be replaced with calculated deflators and there will be an adjustment for late returns from the survey.

There will be revisions to the final quarter figure. The estimated deflators applied to the latest current price data will be replaced with calculated deflators and there will be an adjustment for late returns from the survey.

An upward revision could quite possibly put the final quarter more or less on a par with the previous quarter.

Even without that, looking to the positives, growth of 2.8% in construction output in 2011 is quite something and definitely a bonus for an industry under pressure.

Many (including me) felt the inevitable second dip into recession would come earlier. But these figures show the private sector performed better than many expected. Also the public sector has been far more resilient than expected with the effects of the stimulus longer lasting and the cuts slower to materialise.

This helpful effect, however, will dissipate. The cuts will bite and potentially more aggressively given the level public sector construction has maintained over the past year or so.

Certainly there are clear signs in the output data that the public sector is declining increasingly rapidly.

This will leave the industry increasingly reliant on the private sector to fill the gap left by retreating state funding and to provide any hope of future growth.

Here we see in the latest output figures the worry that has forecasters penning in falls in output this year and next.

While the private sector has done better than many expected a year or so ago, with the exception of infrastructure, growth appears to be flattening out.

Infrastructure remains strong and is contributing to growth. But the other big new work sectors of housing and commercial are showing little signs of rebounding with vigour. Indeed the figures suggest that private house building activity has actually been in decline over the past six months.

This all points to a likely decline.

The lacklustre momentum within construction industry is evident in various industry surveys.

The construction survey by the surveyors’ body RICS tends to provide a bit of a lead indicator of what is likely to happen to construction output. This shows workloads among its members sliding slightly in the third quarter of last year and more significantly in the final quarter.

The rather meagre joy there is to be found by the industry in that set of figures seems to centre mainly on commercial activity in London and the South East.

Of greater concern, perhaps, is the latest ONS data for new orders won published last year. The level of new work has remained subdued which rather undermines hope of enough work making its way through the pipeline to lift construction output in the year ahead.