It’s time for Shapps to find a big bazooka

In September 2010 Grant Shapps set a “Gold Standard” against which he, as housing minister, would be judged – to see a house-building rate at least matching that achieved before the recession.

There are few targets (political hostages to fortune, perhaps) discernable from the reams of documentation and hours of speeches and statements made by this Government.

But this is one. It is important. The consensus is England needs more homes. Sorry, a lot more homes, more even than the previous administration was delivering.

The Gold Standard equates to delivering 175,500 new homes in England a year, or 48,440 in a quarter, depending on how you interpret it. Building fewer would be a failure.

From where we are, with completions running at about 106,000 over the 12 months to September last year, that looks ambitious.

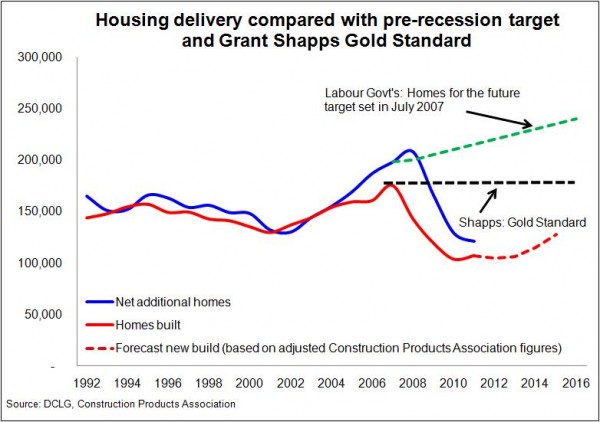

Few, including me, think that target will be met. I have put together a graph showing the rate of increase in housing stock, the current levels of house completions with a forecast from the Construction Products Association (adjusted). I have overlaid this with the previous Government’s target for increasing the housing stock and the Shapps Gold Standard for building more homes.

Few, including me, think that target will be met. I have put together a graph showing the rate of increase in housing stock, the current levels of house completions with a forecast from the Construction Products Association (adjusted). I have overlaid this with the previous Government’s target for increasing the housing stock and the Shapps Gold Standard for building more homes.

By 2015 when the General Election is due the gap between the forecast and the Shapps Gold Standard is about 50,000. That’s to say the industry would need to be producing 40% more than is expected.

This forecast was made after the Government released Laying the Foundations: A Housing Strategy for England.

So it looks like Shapps will need to bring a big bazooka out of his locker if the Government is to avoid a spectacular miss of one of its few stated targets.

Before considering what the bazooka might look like it is worth looking at the current strategy.

Naturally, as with all things New Conservative, the document is pretty much free of targets and detailed numbers of what each policy is expected to achieve in what time frame. In truth the document is less a strategy than a collection of initiatives. Some new, some old, some borrowed…

But there are aspirations and suggestions of the impact that this administration reckons some of the measure will have.

I have tried to add up the implied impact of the various initiatives by taking at face value the claims and delving into the byzantine mathematics and logic that lies behind the impact assessments.

My simple adding up produced a figure for additional homes created each year of more than 100,000. I may be wrong. But, then again, I didn’t add in the impact of renegotiating section 106 agreements and reducing the regulatory burden.

To get a scale of the potential impact of renegotiating S106, in the financial year 2007/08 deals worth roughly £5 billion were agreed. Deals in the previous financial year came to £4 billion. Even a relatively small cut in this burden on developers could, in theory, unlock a host of stalled schemes.

Set the potential reductions in costs against current construction turnover from building new homes of less than £15 billion a year and impact seems potentially huge, leaving aside probably cost savings from reduced regulation.

So, taking the strategy at face value it would seem the Gold Standard is well within reach.

The trouble is few people actually think the strategy will have that great an impact on house building numbers. Certainly not the industry forecasters.

It will however support house building firms, because it focuses mainly on reducing the various burdens and barriers to private sector house builders and developers.

Shapps would most likely argue differently, pointing to increases in affordable housing. There is after all the nth redefinition of “affordable”. This will (in stripped-down terms) mean rents covering ever more, if not all, the cost of financing new build.

And there is the promise of a one-for-one replacement of additional homes bought under a more enticing right-to-buy regime.

Critically, though, it will be the performance of the private sector that will determine whether Shapps gets Gold or the wooden spoon.

Certainly, there is a good argument for focusing on private sector house builders. The private sector delivers the vast majority of homes built in Britain and has, through section 106, provided a large swathe of the social and affordable housing in recent years. Even over the past few years when social housing grew relatively strongly, the private sector delivered more than eight out of ten new homes. So a well functioning private sector is essential.

However, there is a flaw in the plan. The idea that the private sector will double its build rate in four years is beyond ambitious.

Leading up to the recession the major house builders, and other developers, geared up for growth. The industry was accelerating, only to be tripped and, but for the intervention of the previous administration and support from the banks, it would have suffered worse than it did.

As it was, in the wake of the crash, the senior executives of major house builders probably expended more energy renegotiating their finances than building homes. This is not an experience, I suspect, any would want to repeat. Who would?

Talk to most in the business and they would be very happy with annual growth of 5% to 10%. You would not expect them to hunger after growth. It is not their job, nor the responsibility to their shareholders. Their focus is prudently on rebuilding their shattered profit margins, not on growing turnover.

Even at a growth rate of 10% the Gold Standard target would be missed. And it is instructive to know that even during more prosperous times that level of growth has not been sustained. If we look back as far as the 1960s the most growth achieved in private housing completions in England over a four-year stint since was 41%.

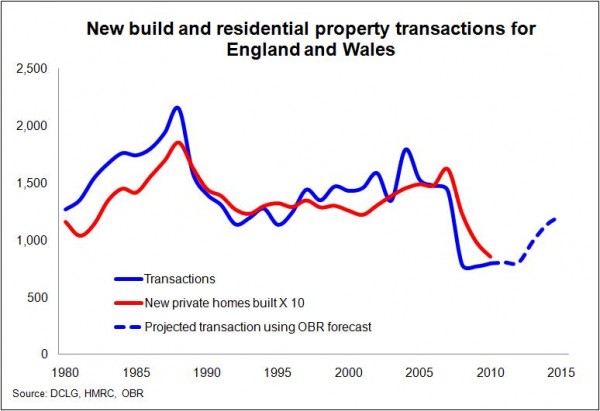

Furthermore there is a relationship that has held since the late 1970s which suggests that for about every ten homes sold one is new. With transactions low and unlikely to rise this suggests that this relationship would need to be broken if we are to see any great growth in private sector completions as the graph shows.

Furthermore there is a relationship that has held since the late 1970s which suggests that for about every ten homes sold one is new. With transactions low and unlikely to rise this suggests that this relationship would need to be broken if we are to see any great growth in private sector completions as the graph shows.

The housing strategy has shifted the balance in favour of new homes, this may change the relationship. But as long as homes in the private sector are sold at prices set in the second-hand market, the likelihood is that gains will be taken by developers as greater profit more than through greater volumes.

So what is Shapps to do?

It seems to me that the private sector, even making a valiant effort, is unlikely to come to his rescue. Meanwhile the public sector is not a real option. It’s skint and the Government is fixated on deficit reduction.

There is, however, one third option. The bazooka.

The Government could encourage the Bank of England to stump up the liquidity to float the house building industry through this period of troubled times using its Asset Purchase Scheme (quantitative easing).

It has been encouraging to see this notion getting a wider airing than in posts on brickonomics or Jules Birch’s inside edge.

Yesterday, The Guardian suggested QE might fund social housing. And in the Financial Times representatives of Occupy London pushed the case linking QE to house building in a piece that perhaps surprisingly bigged up the Austrian economist Hayek, a darling of many on the right.

While the need for more truly affordable housing is not in doubt, limiting the notion to social housing might prove quite problematic and technically at odds with QE.

The critical issue is that we need to build more homes, whatever the tenure when created.

How might such a scheme work?

I have considered this before, although I’m no expert on the detail. But here is what a stylised version might look like. There will be other and better ways to tap QE for housing I am sure, but this is one suggestion.

A not-for-profit Public Interest Company (PIC) financed by bonds is established.

The PIC has a remit to develop housing, with basic criteria set for sustainability, and with its emphasis on the development of publicly-owned land. It may also need to assist in funding and delivering other aspects of community-essential infrastructure.

The bonds would be bought through the Bank of England Asset Purchase Scheme (APS) with created new money, say £50 billion.

These bonds would be indemnified by the Treasury as are other Bank of England APS interventions.

The PIC, as a financing body, would fund and deliver housing in partnership with others, contractors, developers, social housing providers etc. There would be a close relationship with the Homes and Communities Agency.

Getting the tenure mix right would be critical to success. Innovation would be needed in developing tenure models and a mix that is consistent with a sustainable community. But largely the housing tenure it would fund would be predominantly rental-based (possibly with options to buy) and shared ownership/equity. It would not be there to compete with the private sector, but to collaborate.

Very importantly, the PIC should also have a remit to develop suitable stock designed and ready for future sale off-the-shelf to institutions. This would represent an opportunity to kick-start greater institutional investment.

The rental incomes and other incomes would fund the coupon on the bond.

At a suitable point the Bank of England would sell its bonds in the PIC and metaphorically burn the money.

The PIC could then be continued, refocused or wound down, treated as a body similar to the former Commission for the New Towns.

The exact structure is not the point. What is essential is that this process takes place now while the nation, and particularly the construction industry, is in a slump.

Why?

Because in a recession the economics of such a scheme, viewed from a Treasury or national perspective, are vastly different than during a period of growth.

During a recession such an intervention can save the nation billions of pounds and contribute to reducing the deficit. It creates employment from the unemployed and stimulates other activity. It generates taxes. It injects liquidity where it is really needed. It also reduces house price inflation come the next up cycle.

And the important bi-product is more people with a decent place to live in.

On my calculations, for every home built during a recession when industry unemployment is high the Treasury is £20,000 better off. That’s £2 billion if you build 100,000 extra homes. That takes no account of the much-talked-of multiplier effect associated with building.

The potency of house building should not be underestimated.

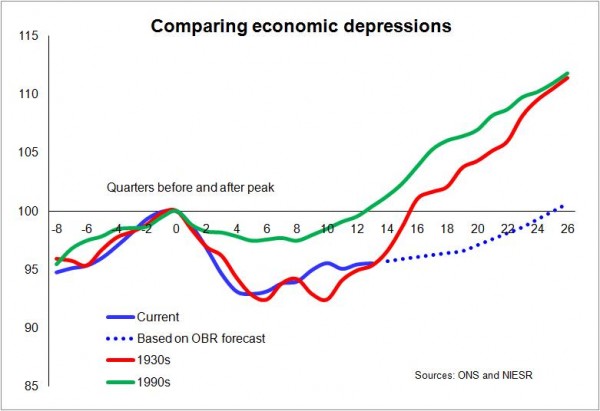

Let’s look to history. Here’s a graph of past depressions (periods when GDP remains below the previous peak).

The graph shows we are at a critical point of departure when compared with the 1930s. At this point in the cycle of depression, our 1930s forebears were seeing an accelerating economy.

The graph shows we are at a critical point of departure when compared with the 1930s. At this point in the cycle of depression, our 1930s forebears were seeing an accelerating economy.

Why?

They were building more homes than ever before, driven in large part by a private housing boom, based on cheap money and cheap land. There was also a surge in public sector house building.

The private sector will not and oughtn’t to attempt to grow in such spectacular fashion. The public sector can play a role, but it is limited.

Something else is needed.

It seems that when nations look for a big bazooka these days they look to central banks. So why not look to the Bank of England and quantitative easing?