The dials are set for a long period of flatlining but high house prices that bodes ill for building

The latest batch of housing market indicators show no real sign that the UK market overall is either collapsing through concerns over the economy and jobs or rising on lack of supply. The pattern continues of house prices gently sliding nationally.

But as the latest report released today by the surveyors’ body RICS shows London remains, in the eyes of estate agents at least, a completely different market to the rest of the UK. In London a positive balance of 25% of surveyors saw price rises, while nationally the figure stands at -23%.

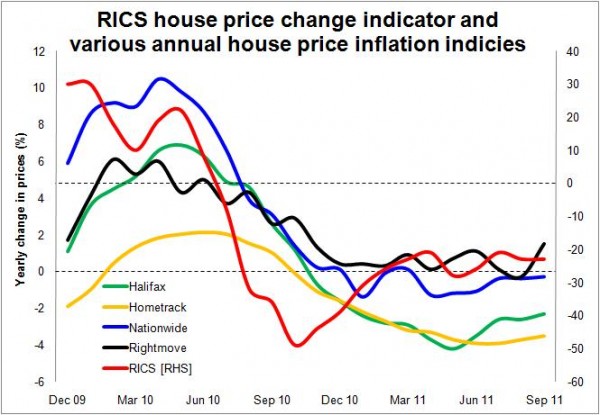

The graph shows that a range of indicators showing the direction of prices paid for homes is mildly negative, while the Rightmove series of asking prices did move positive in September.

The graph shows that a range of indicators showing the direction of prices paid for homes is mildly negative, while the Rightmove series of asking prices did move positive in September.

It is silly to put too much emphasis on monthly figures, because of the skittishness of the market. If one were looking for an explanation for the positive shift in asking prices one might also look to the RICS survey which found sellers were thinner on the ground, a finding that was echoed in the Hometrack survey.

It is reasonable to assume that the sellers that withdraw from the market will on average be the less bullish, so pushing up the average asking price.

Meanwhile, Hometrack and the RICS have come out with contradictory findings, on the month, regarding the change in buyers. Hometrack recorded a fall while the RICS data suggests a slight rise.

But in reality these minor changes month to month tell us little.

Hometrack, however, has looked at the shift in supply (those actively looking to sell) and the demand (those actively looking to buy). Its analysis suggests that while supply has grown 22% demand has risen just 11% over the first nine months of the year.

Its view is that uncertainty over the economy both at home and in Europe is likely to dent confidence further resulting in demand slipping further.

There are of course other possible takes on the current economic weakness. The Bank of England returning to quantitative easing does point to interest rates staying very low for longer. This might for some wavering potential buyers be a trigger to buy rather than rent.

Either way the figures remain unhealthy and this is a market badly suited to expanding the numbers of homes built. The Home Builders Federation monthly survey shows more house builders cutting prices than increasing prices and more use of incentives.

Looking further forward the picture still looks grim, if we choose to use financial market data as a guide.

Residential derivative deals, as measured by Peter Sceats & Associates Future HPI, point to a fall in the price of houses over the next two years of about 5% in cash terms. Even if inflation eases that suggests a double-digit real house-price fall.

More worrying is the perception of house prices in the long term. Buyers of derivatives are prepared to bet that house prices in 10 years time will have risen just 1.7% on average a year since 2010. So they are booking in a real-term fall in prices over this decade on the assumption that inflation will be higher than 1.7%.

Looking at prices further out the numbers suggest an average inflation in house prices of 2.5% over the next 20 years and 2.6% over the next 30 years.

It would be wrong to read too much into the market prices for future housing, as these deals will often be part of a mixed portfolio of investment decisions, so how much is a hedging position and how much is a real view of the future market is hard to establish. But it remains indicative of how the markets see housing and house prices in the future.

As Grant Shapps regularly says there is great value in stability in house prices. The problem however is the starting point.

Relative to earnings house prices are historically high and the affordability of housing is flattered by exceptionally low interest rates.

With low earnings growth expected over the next few years and little build up of equity as a result of low house price growth and recent falls in prices, the prospects for an increase in transactions looks dismal.

If we are looking at low levels of transactions for many years to come this bodes very ill for house building. Traditionally the level of sales of new homes runs in near parallel with the level of overall sales on a ratio, broadly one to ten.

If this relation holds we face being condemned to low levels of private house building for many years hence.