Housing market seems to be entering a new phase as economic worries grow

The housing market survey released today by the surveyors’ body RICS adds to other recently released data that all seems to points to a slide in prices everywhere except London – which in housing terms is another country.

The RICS data show a negative balance of 23% of those questioned suggesting prices were falling rather over the past three months above those that saw prices rising.

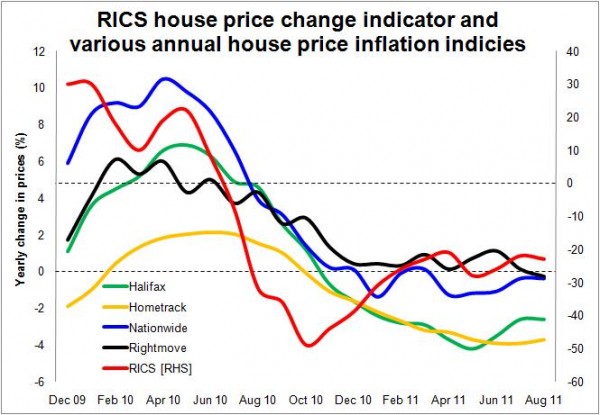

This fits with most other house price indicies which suggest that prices are tracking lower now than a year ago and are sliding gently down (see graph).

This fits with most other house price indicies which suggest that prices are tracking lower now than a year ago and are sliding gently down (see graph).

This will no doubt unsettle a few sellers here and there and cheer up those eager to get a firm grip on the of-late greasy ladder of homeownership.

Taking the data as a whole there are signs that we may be entering a new phase in the housing market, as the real impact of the recession bears down on households and their aspirations across the board. This is pretty much in line with the interpretation of the RICS, which found its respondents most frequently citing economic uncertainty as a main factor depressing activity.

How this will play out is very hard to gauge and certainly we can only guess how the Government and lenders will respond if the market does takes a nasty turn.

As things stand, while prices may be softening, there appears to be no reason to panic about an impending price collapse. That said, the RICS figures show the sales per surveyor falling, which may well increase (albeit subtle) pressure from estate agents on sellers to drop their prices in the hope of attracting more buyers and generating more sales.

But for me the greater concern, certainly for house builders, the construction industry and the nation at large would seem to be a potential further drop in transactions. This in turn would most likely lead to a further drop in private sales – all other things being equal.

Now in reality the market may all blow up in our faces. We may see prices rise again. Who knows? I don’t.

That uncertainty over the market and the difficulty in reading it is evident in the varied interpretations by those who profess expertise in the area of house price projection. Most, in fairness, have pretty much nailed the year to date with their predictions for this year being a gentle fall in prices.

Certainly, what has been intriguing over this recession is how adjustments in supply, demand and price have worked out. And not as one might have suggested in early 2007, if asked what would happen to house prices if we were hit by the biggest financial crisis since the 1930s.

Yes prices did plunge when the credit crunch bit, but they have in many parts of the UK recovered quite a bit. And in relation to earnings prices remain extremely high by historic standards.

Certainly in the 1990s we saw demand fall sharply and while supply readjusted a bit, the flood of repossessions on the market boosted it and drove down prices.

We really haven’t seen that mechanism at work this time, at least not on a national level. Instead we have seen supply dropping more or less in line with demand. And when house prices fell substantially we saw supply withdrawn from the market – and prices rose again.

There are two good reasons for this.

Firstly mortgage rates plunged. This reduced the stress on mortgage holders and lowered the number of repossessions and forced sales we may have expected. It also made it easier for people to hold onto properties they no longer wished to live in and rent them out instead in the hope of securing a better price later.

Secondly, we saw far more leniency from the lenders and a Government keen to help to avoid a spate of repossessions. As well as the natural human concern, the banks had a greater vested interest in supporting house prices this time around – their huge stakes in house builders and land banks which would be badly hit if house prices plunged.

There will have been other reasons. But the upshot is that we have seen far more stability in prices than we might have hoped for.

But while stable prices is the upside, the downside of this pattern is that transactions have been very low and look like staying low for some while yet.

Furthermore, those that have been buying and selling have been atypical of the market as a whole – well certainly atypical of the market as it was in the decade or so before the credit crunch. Buyers have tended to be better off and with large deposits. Many who might in earlier years have expected to buy are now unable.

This is not encouraging and while this bizarre market continues we are building up potential problems for delivering good housing to all the good people of this nation.