Budget provides a shot in the arm for housing work, but there’s a sting in the detail

A shot in the arm, said the Home Builders Federation release sent out after Chancellor George Osborne sat down.

And the Budget certainly lifted the already rising share prices of the quoted builders quite nicely.

It must be said that comment came as no shock, as this was yet another ask or two or three by house builders that have been favourably answered by the incumbent Government.

Putting in a presumption in favour of sustainable development in the planning law with the default set to “yes” and the introduction of a re-badge of the HomeBuy Direct scheme under the FirstBuy label was always likely to prompt house builders to pop corks.

And what else the house builders know is that there is a pile of other favourable initiatives working their way through the system that should lighten the burden of regulation – their job now is just to keep the pressure on the Government so that it delivers.

All looks rosy.

But for all the joy there is one sting in the detail within the Budget. The effects of inflation. Sadly people’s earnings are expected to be rather more squeezed than was predicted a year ago by the newly established oversight quango the Office for Budget Responsibility.

But for all the joy there is one sting in the detail within the Budget. The effects of inflation. Sadly people’s earnings are expected to be rather more squeezed than was predicted a year ago by the newly established oversight quango the Office for Budget Responsibility.

Still, back to the good news bit. The Government reckons that the FirstBuy programme will help about 10,000 first-time buyers buy a home. That makes it about the same scale as the HomeBuy Direct scheme, but a shade less generous.

It will provide a £250 million pot to take 10% equity stakes to match 10% stakes held by the house builders and 5% stakes held by the buyers of the new homes. This will provide the magic 25% equity stake deposit that should release more home loans and so boost sales to first-time buyers and, for some, reduce their loan payments.

There is the obvious question of how much of an extra boost this will provide, given that a portion of those taking up the deal would probably have scraped a deposit together anyway.

I guess it will certainly prompt potential buyers to look harder at buying new-build rather than second-hand homes, which will in turn have some distorting effects on the market.

The other factor that needs to be taken into account when assessing the impact of this initiative is the willingness of lenders to take on their books those they feel might struggle to meet payments if interest rates rose. The lender Santander made that warning as soon as the initiative was announced.

But for the Government it has to be a no-brainer. The money it puts into supporting the purchase of a new home is not lost, as it retains an equity stake that can be recycled later.

Further, it will probably cut its benefits payments and increase its tax take by the tune of between £10,000 and £20,000 for every new home that is built, by taking construction workers off the dole. That is not taking account of other multiplier effects.

Meanwhile, within the Budget there was plenty more for the builders of homes to be cheered about. The removal of the 2% conversion charge for real estate investment trusts (REITs), may incline more property firms to convert and may just help to open more opportunities for investment.

Also a stamp duty hurdle that irritated institutional investors is being removed. Stamp duty used to be payable on the bulk purchase of properties. Inevitably when lots of properties were bought that would mean the top rate of 5%. Now the charge will be on the mean value of the properties, which in most cases will mean paying a lower rate of stamp duty.

And then there were the more developer-favourable announcements within the Budget speech on planning and more noises about reducing burdens on business.

Although in reality many of these changes to the planning system will take a while to filter through to help boost construction work.

Perhaps of more immediate concern is how flush potential homebuyers will be when they come to look at the FirstBuy option or any other opportunities to buy a home.

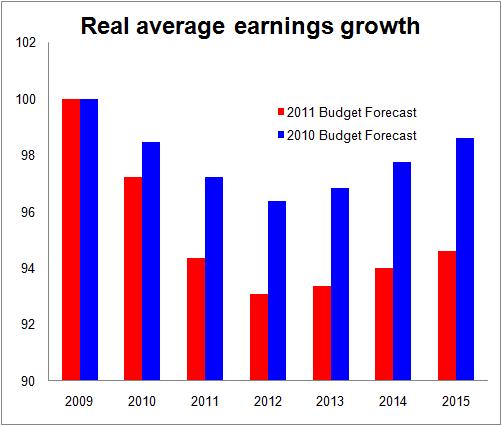

What received little direct coverage was the implicit squeeze of earnings and the implications that has for both house building and, particularly, for residential repair and maintenance.

I have put together some crude calculations of real earnings growth taken from the forecast figures produced by the OBR in the latest Budget and compared them with the previous budget (see graph above).

If we start from a base of 100 in 2009 and use the use the RPI measure of inflation to adjust nominal average earnings to real earnings, we find they are expected to fall to about 93.1 by the end of 2012. This compares with a figure of 96.4, if you do the same calculation with last year’s forecast.

You can use the CPI measure or deflate using the GDP deflators, but what these crude figures show is that what was always looking like a nasty squeeze on households now looks that much nastier.