Why the forecast of a shallower recession is bad news for contractors

The latest forecast from the Construction Products Association suggests that the drop in future workload will not be as large as the forecasters had previously thought.

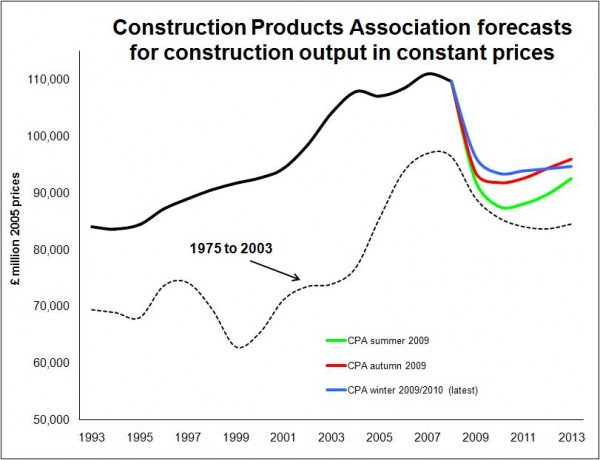

The graph opposite compares the past three Construction Products Association forecasts.

The graph opposite compares the past three Construction Products Association forecasts.

It clearly shows that with each progressive quarterly forecast the expected hole in construction workload has shrunk.

Fantastic news you might think. Well think again.

If you’re a contractor this is probably bad news not good news.

And here’s why.

Much of the apparent improvement in the prospects for construction output rest on the changes to the deflators applied by the national statisticians.

The deflators are used to convert current prices, or the cash construction has brought in, into constant prices, an estimated measure of the volume of work done unaffected by changes in the price of the work done.

It is clear from the revisions to recent output figures that the statisticians now think that contractors are getting less for the work they have done than was previously estimated. That is to say that construction prices are falling faster than first thought.

This has led to a revision upward in the constant price data (the volume of work done) while the current price data (cash netted by the construction industry) have remained the same.

This means that in the statisticians’ view contractors have been doing more work than previously thought, but for the same amount of money.

A look at the figures shows that, in the revisions made when the third quarter 2009 figures were published, almost £700 million was added to the amount of work done in the first quarter even though the amount of cash earned by the industry remained the same. At the same time the release showed an upward revision of the second quarter constant prices data of almost £600 million.

Given this the forecasters will have had to factor this in and taken a much tougher view on when making their estimates for future prices.

Little wonder then that the Construction Products Association has progressively raised its estimate for 2009 construction output in constant prices by about £4 billion since its forecast last summer.

No doubt a rise in volumes is probably good news for the materials supply industry. But if you are a contractor and still reading this forecast as good news, here is a question you might want to ask yourself. What is better for a contractor: to see prices drop 5% and workload drop 15%; or to see prices drop 15% and workload drop 5%?

In truth the adjustments to the deflators does not appear to account for all the upward adjustment in the Construction Products Association forecast.

There will always be adjustments to forecasts and particularly when we have a Government pulling forward capital spending.

And there has certainly been s an improvement in the sentiment of the forecasters at the Construction Products Association with respect to the level of workload in the short term.

But this short-term improvement probably doesn’t outweigh the much bleaker view the forecasters have of recovery.

The longer-term projection suggests that construction may be trapped in very low growth for many years to come, that’s if it does not slip into a double-dip recession.