Housing market picks up speed, but where’s it heading?

Whatever measure you use for house price inflation the figure for 2013 seems increasingly likely to be closer to 10% than 0%. At least the latest (November) HM Treasury Forecasts for the UK economy puts the median of the forecasts it compared at 5.9%.

This would not be exceptional growth, but pretty strong given that a year ago more forecasters (on my reckoning) expected house prices to stagnate or fall than to rise.

These were sound forecasts with the economy wobbling, household finances squeezed and the Eurozone crisis bubbling nastily. (You can get a clue of the numbers and the backdrop from this blog in January)

But the nature of things is to throw up surprises – how many predicted England to lose the first two tests in the Ashes?

The important lesson here, though, is less that surprises happen and more what lies behind them and what they might mean for the future.

The important lesson here, though, is less that surprises happen and more what lies behind them and what they might mean for the future.

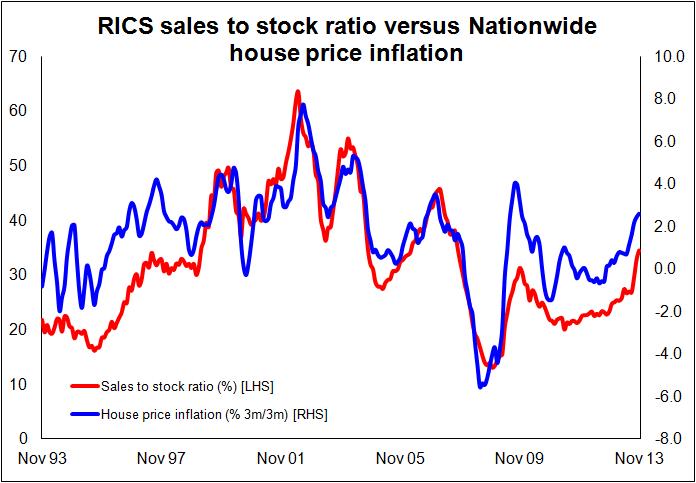

To get a feel for where we are and where we appear to be heading the RICS housing market survey out today provides clues. It shows signs of further house price inflation. Stocks seem to be dwindling as sales rise, inquiries (potential buyers) rise and new instructions (potential sellers) stagnate.

The wonderful RICS sales-to-stock ratio gives a clue to the likely direction of prices when this happens. (The chart compares the ratio with Nationwide’s moving 3 month/3 month house price inflation)

That suggests more upward pressure on prices and it is fair to say that is consistent with most of the more recent forecasts, including that from the Office for Budget Responsibility. It, interestingly, has built its own house-price inflation model.

OBR is expecting inflation this year of less than the consensus at 3.2% followed by 5.2% in 2014 and 7.2% in 2015.

So we seem to be in the territory, if the forecasters are right, of house prices rising far faster than incomes.

Looking at the things that drive house building, house price inflation generally helps in the short run at least.

But the thing that seemed to have been uppermost in the minds of the builders a year or so ago was mortgage terms and availability and buyer confidence. These figure as constraints far less now than then, according to the latest Homebuilders Federation survey.

Indeed the constraints have shifted quite markedly from sales to production.

Moving away from house prices, the Council of Mortgage Lenders provides its forecast today. This looks more at the mortgage market and transactions. And the data it provides pretty much explains the more relaxed view house builders have over sales.

The message here too is positive in comparison with expectations a year ago. It sees more residential transactions than expected this year, about 10%.

This is good for construction as more turnover of the overall stock in market generally leads to more house building.

It also sees a rise in gross advances, which suggests a more fluid mortgage market. And overall it paints a fairly positive picture for the next two years.

So looking at all the available data, the house building fraternity will enjoy its best Christmas for many a year.

But for me, the CML forecast makes perhaps one of the most pertinent points and one of the more succinct expressions of where we are.

It says: “This is an interesting time to be publishing market forecasts. There is a strong consensus about the immediate direction of travel for the housing market, but little agreement as to its eventual destination.”

This is a point to note well. We still live in very uncertain times.

The current remedies for the housing market are creating concern and increasing the risks in the system. So don’t be surprised by surprises.

England may just retain the Ashes.