Output falls as construction faces worrying time over jobs in 2013

The latest Office for National Statistics construction output figures fit the pattern of an industry is sharp decline.

There was a brief pause for optimism last month as the October data provided a lift. But I cautioned last month about reading too much into one month’s data and, as Noble Francis at the Construction Products Associate suggests, this rise may well have been down to a delayed post-Olympic surge. Such a delayed impact is understandable, as there are lags in the output data.

Whatever the reasons the November figures put the industry back on its path of decline.

Whatever the reasons the November figures put the industry back on its path of decline.

On an annualised basis the industry has shrunk £6 billion in cash terms since the start of the year and more than 7% in volume terms.

The latest forecasts suggest that we should expect further decline this year after what is looking like a near 9% fall for 2012.

That would make the collapse in construction the fourth worst recorded since 1955. For the record, the worst fall was in 2009, followed by 1974 and 1981.

In fairness there are promising elements to the data. Infrastructure work is buoyant having more than doubled in real terms since 2007. Sadly that just makes the performance of building work look worse.

Hopes of recovery in housing and commercial work have increasingly been moderated. Indeed, the private commercial sector is in decline.

Before anyone gets over excited when the GDP figures come out showing a rise in construction, we should expect to see an increase in Q4 output, say about 3% or so quarter on quarter. Indeed NIESR seems to be working on an estimated increase of more than 4% q/q for construction in the final quarter, which may prove a bit strong given today’s figures.

This likely rise may well be seized upon by some as a sign of revival in the sector. It will not be. The path of construction output tends to be bumpy during periods of change and we experienced some horrid bumps in 2012.

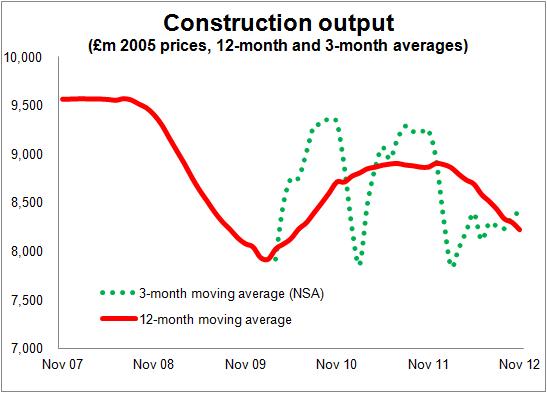

These bumps in part were exaggerated by unusual seasonal and one off effects. As the graph illustrates the late summer surge in output (see green dotted line showing three monthly average) did not occur this year. So this lower base should help to flatter the output figure in the final quarter

While we should see fewer bumps this year (hopefully) the real story will be how the 2012 collapse in output feeds through into job losses.