Beware estate agents selling optimism – the housing market remains in a worrisome state

There was a very upbeat headline given by the RICS press office to the latest housing market survey released today by the surveyors’ body.

Judging by various headlines from news outlets, including that on the BBC website, and various tweets I noticed on the subject, the message received by the casual observer appears to be “well that’s all good then”.

I was bemused.

I can see that less bad may be construed as good in a world of torture. But looking at life in a broader context the best we can say about the housing market is that it might be a bit more stable at an awful level as we end this year.

I can see that less bad may be construed as good in a world of torture. But looking at life in a broader context the best we can say about the housing market is that it might be a bit more stable at an awful level as we end this year.

Put another way we should expect to see pretty much the same as we have seen over the past two years.

Sales of homes will remain at pathetic levels. The number of houses being built will still be half those needed. Prices will continue to be out of the reach of most young folk. And the homeless and hidden homeless will continue to suffer.

That’s not my idea of a bright end to 2012 for the housing market.

But then again the debate on the housing market is complex, contradictory and frequently confused by the personal circumstances of those observing it.

So, those who own homes tend to favour rising house prices and those don’t own homes almost universally favour house price falls, well at least until they buy one. Those in homes frequently don’t want homes built near them, while those looking to buy or rent new homes normally want them built near existing homes.

Leaving that tub of worms, maggots and snakes to wriggle on one side, what are the grounds for optimism within the RICS press office?

They appear to be that on balance estate agents saw a rise instead of a fall in interest from new buyers and that sales expectations among estate agents were very positive.

But even the RICS’s own data shows clearly what we all instinctively know, estate agents have a record of severe over optimism.

Underlying this resurgent optimism seems to be the lifeline thrown by the Government and the Bank of England in the form of the Funding for Lending Scheme (FLS) in mid July.

This as the name suggests is intended to lead to more lending and it would be a hopeless waste of effort if it doesn’t.

But the general view seems to be that its impact will be modest. Certainly that was the view expressed by Hometrack’s Richard Donnell in comments within his latest monthly housing survey and other commentators and experts seem to follow this view.

Interestingly the word “support” seems to be (from my reading anyway) used rather more frequently than “boost”.

There were many telling comments made by speakers at the recent Housing Market Intelligence conference. (Here issues of probity suggest to me I should declare my interest, I edit the associated report)

But on the subject of the FLS comments from Stephen Noakes, Mortgage Director at Lloyds Banking Group stuck out, particularly his take on the counterfactual.

He was clearly irritated by media commentary on the scheme that questioned its impact after such a short time. His view was that it would have a welcome short-term, but indiscriminate impact on the market.

But his more potent message was that things would have been far worse in the mortgage market had the scheme not been put in place.

For me this supports the view that the market remains in a state of unstable equilibrium, even at its current low level.

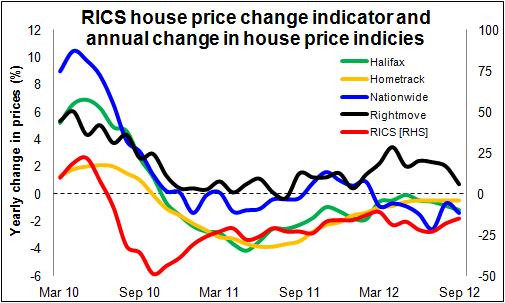

The reality is that the housing market is in a dire state, despite house prices being in the realm of stable to gently falling, as shown in the graph above.

Yes, this provides some comfort to policy makers, who fear the wider impact of rapidly falling house prices on the economy and growth. But this is no comfort to the prospective house buyer who feels left out in the cold unable to access the market at current prices.

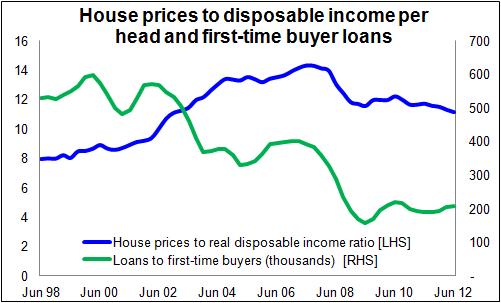

There are many graphs I could have put together to illustrate my point. But for a change I’ve put assembled a graph showing the ratio of house prices (using the Nationwide data) and per capita disposable income from the ONS. I have set this against the home loans for first-time buyers.

There are many graphs I could have put together to illustrate my point. But for a change I’ve put assembled a graph showing the ratio of house prices (using the Nationwide data) and per capita disposable income from the ONS. I have set this against the home loans for first-time buyers.

Now there are many factors driving the first-time buyer market, interest rates, deposits and acceptance being important and having potentially a big influence. We can add into this plenty of other factors such as demographics, geography, family wealth and speculation effects. But in the long run the price of the purchase against the available income underlies all this.

It is clear that as far back as 2003 when house prices rose sharply relative to available income that first-time buyers rapidly dropped out of the market, despite readily available finance, fairly low interest rates and (as we now know) rather lax scrutiny.

As we see we are back to about the same ratio as we were at the start of 2003. That was a level at which FTBs took flight. On that basis it would be a surprise to see a flood of first-time coming into the market and a return to what many see as a more normal market conditions.

So I am afraid that while the RICS may see a brighter end to the year, in relative terms it is still extremely gloomy.

2 thoughts on “Beware estate agents selling optimism – the housing market remains in a worrisome state”

The sheer amount of so-called “house price data” is overwhelming now – very little of which is accurate or any use unfortunately. Surveying the optimism of sellers, surveyors or potential first time buyers is nothing more more than PR – you can’t determine anything useful from it.

Surely they are just whistling to keep their spirits up and hoping if they keep saying there is an upturn then there will be one

Comments are closed.