Renovation and green agenda support weak construction activity across Europe

The Euroconstruct conference held earlier this month in London provided lashings of gloom, but it also provided plenty of food for thought.

The twice-yearly conference brings together the thoughts and expectations of construction economic research groups covering 19 European countries.

I have not been for many years and forgot how useful it was to look at the similarities and differences between countries. Even if you are not that interested in other European construction markets, seeing how they are performing helps to better understand your home market.

Much came out of the conference, but the five key messages that I took home were:

- Things keep getting worse than were previously expected

- The pattern of growth and contraction varies very widely country to country

- There has been a structural shift between new build and renovation work

- Civils is currently suffering more than building

- The green agenda seems to be one of the biggest potential drivers of construction growth

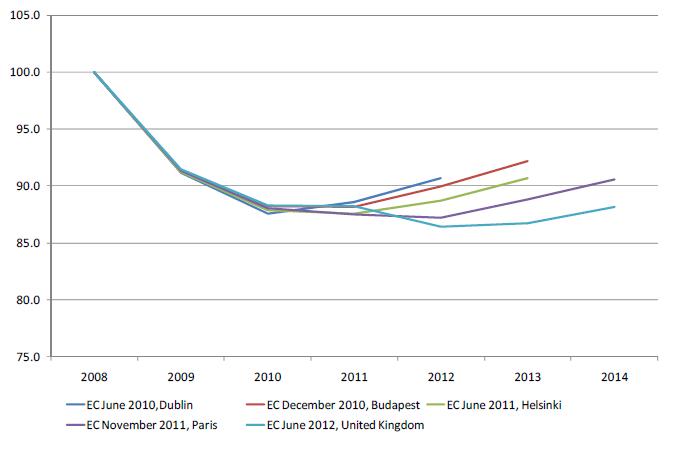

The first graph shows the forecasts for total construction activity within the 19 Euroconstruct countries presented at the latest five Euroconstruct conferences and how since 2010 hopes of recovery have been dashed.

Not only has the expected recovery been consistently pushed into the future by the forecasters, but they have reduced their expectations for the pace of recovery.

Frankly there will be no bounce back in the forecast period and even by 2014 the size of the European construction market is likely to be about 15% smaller than it was before the crisis began.

And it would be a fair guess that these forecasts are more optimistic than they would be if they were made today, rather than a couple of months ago.

A speculative projection made at the conference suggested it may well be 2022 before the European construction industry reaches the level of its former peak.

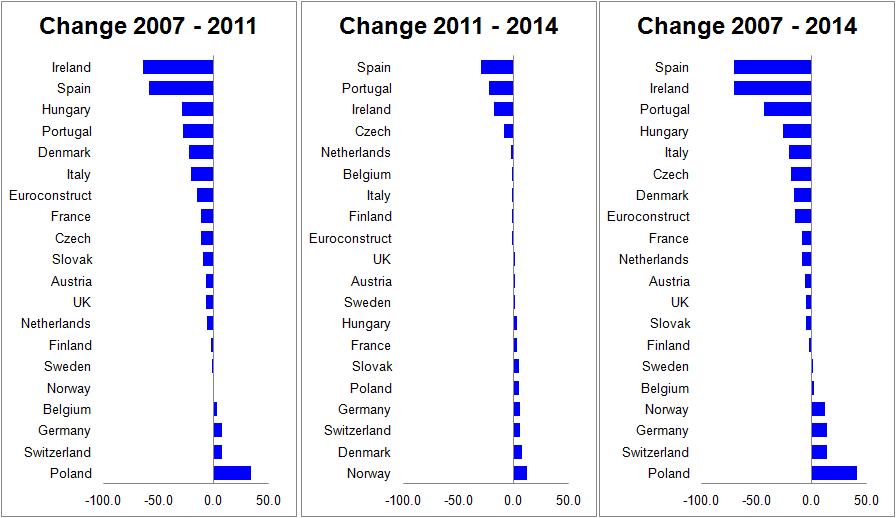

But it is not all doom and gloom across the continent. There is a wide spread in the fortunes of construction markets across Europe, with what might be loosely described as a north-south divide. In Germany, Switzerland and Poland for instance the industry continues to plough on strongly, while the Nordic counties too are looking relatively promising.

And while the UK construction industry has faced a very tough time in recent years, its plight is nothing when compared to others, particularly some of the more southern nations in Europe.

In aggregate terms the overall depressing figures for European construction are greatly influenced by the collapse of the Spanish, Italian and, to a lesser extent, French markets with Ireland a big contributor to the decline despite being a small country.

To put things into perspective by the end of this year the drop in Spanish construction output will be more than the value of the entire UK construction market.

Graph 2 show just how deep the drop from 2008 to 2011 has been for some countries while Graph 3 shows the variation in the forecast prospects. Graph 4 shows the expected change from 2007 to 2014

By the time this phase has played out the Spanish and Irish construction sectors will be about 30% as big as they were in their pre-crash pomp. Downturns on that scale are normally restricted to periods of war.

What is largely responsible for the collapse in these two countries is that massive drop in house building. This has had a big impact across Europe with the amount of new residential construction down by about 40% from the peak in 2006.

Meanwhile new non-residential building work has also taken a hammering, down 20 from peak. And both new civil engineering and civils renovation work have fallen by a shade under 7%. That fall has been in the past couple of years and the expectations are that the sector will continue to contract fairly fast this year, but relatively the renovation side of civils is expected to do better.

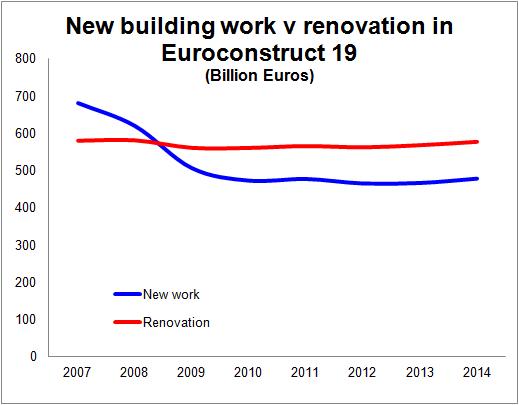

Indeed when we look at renovation work in the building sector, both residential and non-residential, it has fallen far less across Europe as a whole than new work.

Graph 5 shows how relatively flat renovation work in the building sector has been in comparison with new work.

Graph 5 shows how relatively flat renovation work in the building sector has been in comparison with new work.

This is to be expected as new work will tend to rely far more on growth and confidence within the wider economy. These have been clearly lacking in Europe for some while and continue to be.

The definitions vary country to country over exactly what falls into the renovation and new work categories, but the pattern is clear. New work has dropped as a proportion of the total mix while renovation has grown. And the projection is that it will remain for some while the dominant sector.

One big driver of this shift is the green agenda, with increasing work in the building sector to reduce energy consumption.

Meanwhile the sustainability agenda is also expected to be a driver for the energy and water sectors within the civils sector.

So as we see, from a UK perspective, while there are clear and extreme differences in the fortunes of construction at home and in various parts of the rest of Europe there appear to be some common themes.