Glimpses of improvement in housing market, but economic woes continue to dog prospects

There were positive glimpses within the latest batch of housing statistics. But on balance these seem too weak to deliver a recovery sufficient to propel house building numbers given the drag caused by an enfeebled and uncertain economy.

The Home Builders Federation survey showed October to be very significantly better than a year ago for both site visits and net reservations, although both were lower than in September.

The Council for Mortgage Lenders estimate for gross mortgage lending in October was 13% higher than a year ago. But it must be remembered that mortgage lending in the autumn of last year was pretty soft.

Meanwhile the latest housing market survey from the surveyors’ body RICS suggests that November saw more buyers coming into the market.

Meanwhile the latest housing market survey from the surveyors’ body RICS suggests that November saw more buyers coming into the market.

But for all that that is a positive sign, there is little in the RICS figures to suggest a particular upward turning point in the housing market.

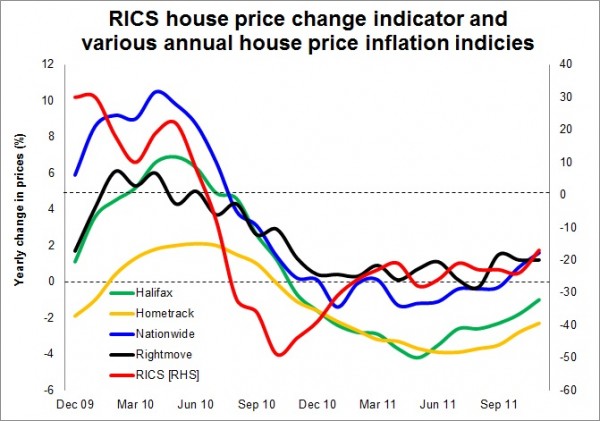

The vast array of house price indicators, on balance, suggests the UK average house price may be rising very slightly. But in real terms prices remain in decline. The general flatness in UK house prices is evident from the graph showing a selection of those indicators.

What the graph does not show is that UK average prices are being buoyed by the more active London market. Much of the country is seeing price falls, a pattern very evident in the RICS survey.

All this accumulated data seems to have propped up sentiment in the City over the direction of house prices.

The latest figures for future prices of housing, as expressed in the Future HPI put together by Peter Sceats & Associates suggests the City traders expects a shallower slump in house prices than it was even a month ago.

But it should be remembered that, in part, this may actually be a reflection of the weakness of the broader economy and the increasing likelihood that interest rates may stay lower for longer helping to sustain prices.

Traders now are pricing in a slump in house prices of about 3% compared with December 2010 prices. Last month the future price suggested the slump may exceed 5%.