Will Tory plans to sell council houses to fund new affordable rented homes work?

Prime Minister David Cameron chose housing as a key theme for his opening shots ahead of the Conservative Party’s annual conference, announcing in an interview with Andrew Marr of the BBC a proposal that he says will create 200,000 new homes.

Central to the policy is promoting the sale of council housing and also passing Government land to house builders on a build-now-pay-later basis.

Among the political and economic advantages to the Government of both these schemes is that in theogy they exploit existing assets and so do not add to the public debt, while they promote growth through stimulating house building.

Each of the two policy elements Mr Cameron reckons will generate 100,000 new homes.

On the right to buy initiative, he argues that by increasing discounts to those who wish to buy their council home more people will opt to buy rather than keep renting.

This, the Government believes, would generate significant sums of extra money and the stated intention is that “every additional pound generated by the sales will be invested in paying down the debt associated with that property and on building new housing for affordable rent”.

Leaving aside the obvious and awkward social, political and fairness issues (such as pawning the family silver, as Lord Stockton might have described it) this approach has raised a number of questions in terms of feasibility and practicality.

Will a rejuvenated Right-to-Buy system actually work as the Government hopes?

This in turn poses other questions such as:

- Will the Government actually stimulate 100,000 extra buyers of council homes?

- How will the money raised be fed into the funding system to build new affordable homes?

- Will the cash stay with the local authority selling the homes or will it be pooled nationally?

The thinking is to be fleshed out in a forthcoming Housing Strategy document and the answers to these – assuming they are provided – will in large part determine how much house building the initiative might stimulate.

I’ll try to explore the first of those three questions here and move on to the other two in a later blog.

It would be easy to dismiss out of hand the idea that a cut in discounts would significantly increase council house sales for a host of reasons: the collapse in sales of council homes recently was pretty dramatic; the likelihood that the cream of the stock has already been sold; the mortgage squeeze; the recession; relatively high unemployment in relation to recent years; the high price of homes relative to earnings; the relative decline of wealth and earnings among those housed by the council, the general pall of gloom over the economy; and more.

But a quick exploration of the figures suggests that this policy might work, albeit with the help of the normal political smoke and mirrors around the figures.

But a quick exploration of the figures suggests that this policy might work, albeit with the help of the normal political smoke and mirrors around the figures.

That said it’s not easy to gauge what extra appetite might be created among council tenants to exercise their right to buy if they were tempted by deeper discounts.

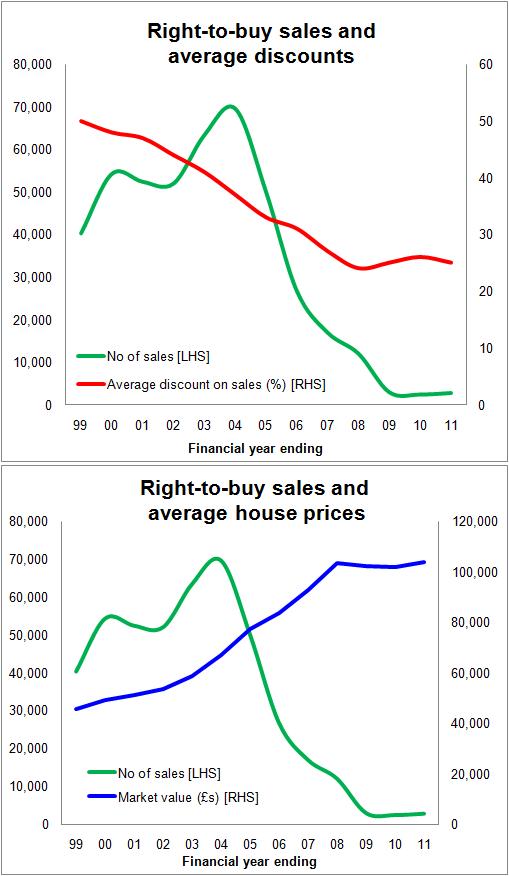

Undoubtedly there will be a link between higher discounts and more sales. But was the collapse in council house sales from 2004 (see graph) simply down to the previous Government lowering discounts as the current Government argues?

The Housing (Right to Buy) (Maximum Discount) Order 1998 which began to restrict discounts came into force on 11 February 1999 and new legislation was introduced in January 2005 that further restricted discounts and introduce new rules on resale that were less attractive to would-be buyers. And there were other tweaks to the system.

The effects of the restrictions on discounts are clear in the official figures. At the end of 1990s discounts averaged 50% of the market value of the homes sold. This dropped to 24% in financial year to 2008.

However despite decreasing average discounts sales continued to rise through to the financial year ending 2004.

In that financial year almost 70,000 sales went through under the scheme in England generating almost £3 billion in capital receipts on the sale of homes estimated to be worth £4.7 billion.

This is not a patch on the near 200,000 sold in 1982, but in 2004 council homes were being sold at a higher rate than at any point since 1992.

This suggests that reducing discounts was probably not the only cause of the fall in council house sales.

A further factor in the slow down in sales of council housing after 2004 is likely to be the pace of house price inflation, which will have taken the homes of would-be buyers out of their reach, particularly as discounts reduced in proportion if not in cash terms.

More recently the recession and the housing market collapse will have been a major factor, particularly as this will have hit prices in “less desirable” areas harder.

Certainly the recession of the 1990s saw a collapse in council housing sales by more than a third from a peak of 181,000 in 1989 to the mid 1990s.

This all poses the question of how much discount would be needed to raise council house sales dramatically (as is the policy objective) against the headwinds of high house prices and uncertainty over the economy and the future direction of house prices.

The answer would seem to be very deep discounts, particularly in more expensive areas such as central London. But that may be part of the plan to be revealed in the Housing Strategy.

There are of course other factors that may come into play. Controversially, the Government may decide to relax the resale rules permitting quick sales by council house buyers. This would stimulate those looking for lower-risk speculative gain. And no doubt the Government’s desire to see higher rents paid by the more affluent social housing tenants may also shift the balance in the minds of those with the greatest wherewithal towards buying.

There have been questions raised over whether there are enough council tenants with the wherewithal to buy their homes given the social mix within the local authority housing.

Here prejudice and political propaganda plays its part in influencing our expectations. The notion of council estates packed to the gunnels with feckless youth with dissolute parents is, unsurprisingly, rather misleading.

Yes, there are proportionately fewer of the “household reference person” in full-time employment according to the English Housing Survey Household Report 2009/10. The figure for local authority housing is put at 23.1% against 51.5% for all tenancies.

Interestingly, though, the proportion of in full-time employment among local authority tenants appears to have been reasonably stable for a few years, having fallen through the 1980s. In 1981 it was 43%, in 1984 it was it was 31%, in 1991 it was 25% as it was in 2000 and it has been roughly between 20% and 23% since then. Meanwhile, there has been a rise in the proportion categorised as in part-time employment since the 1980s.

It is true that earnings have grown less among those residing in local authority housing than the population as a whole.

But on balance, while relatively low levels of full-time employment among council house folk might restrict the potential enjoyed by the right-to-buy scheme in itsheyday, it would seem unlikely that it would be reason enough to scupper plans to boost right-to-buy sales above the very low levels we see today, although fear of unemployment might play its part.

And, secured on the basis of a full-time job, one must assume that with significant discounts to market value the mortgage lenders would be happy to providing finance on the homes.

Indeed the willingness of lenders to lend on council property will have been much increased by the £30 billion or so investment through the Decent Homes programme over the past decade. This has markedly improved the stock.

It is worth noting too that the proportion of retired folk living in council housing is higher than average. It is not inconceivable that, given sufficiently deep discounts, a proportion of these may be tempted to buy their homes with assistance from their adult children as a means of creating family wealth.

Mr Cameron suggests the policy would create sufficient interest to generate about 100,000 more sales, one assumes over the approximate three years from when legislation might be introduced to the end of this Parliament.

This suggests about 35,000 sales a year, which in turn suggests we are looking at levels of sales at about two thirds of those achieved in the first half of the noughties. That represents about 2% of the existing council housing stock of 1.8 million homes sold each year.

It is dangerous using averages because of the huge regional variations in earnings and house prices, but for simplicity let’s look at the average valuation of the average council house sold in England in the past financial year was £104,000, according to DCLG figures.

The average discount was £26,500, suggesting a price paid by the former tenants of £77,500. This was a rise of a third from the cash needed to buy at the 2004 peak.

Deepen the discount to 50% and the price paid by the tenant would have been £52,000, which easily brings into scope those earning £20,000.

According to the English Housing Survey, the proportion of social renters (this includes housing associations, which have a similar tenant profile to local authorities) with a gross annual income from the household reference person and partner of more than £30,000 is about 9% to 10%. A further 14% or so have an income of between £20,000 and £30,000.

Clearly the distribution of earnings and house prices is critical in determining how many folk would come into scope, but there does seem to be a reasonable slice of council-housed households that would earn enough to get a mortgage. Add to this, I suggest, a proportion of the 30% or more of the households that are retirees and there is, potentially, sufficient numbers with the capacity to buy to meet the “target” of 100,000, providing the discounts are deep.

And if the discounts are deep enough the financial case to buy starts to look more attractive. The median rent in 2009/10 is calculated at £67 per week, which works out at about the same cost as a 25-year repayment mortgages at 5% on £50,000.

Furthermore the Government has other tempting elements it could add in to sweeten the pot, such as reducing the resale embargo period and/or providing full-rate guaranteed buy-backs during that period for those that get into financial trouble having bought their home.

Playing up fears of housing shortages and access to housing would also create mood music sympathetic to buying into housing rather than renting.

So put it all together and you can see why the Government might think this will work and potentially in the numbers suggested.

That then leaves the question of how much will it raise and how will it be spent to create an equal number of affordable rent homes?

That I’ll consider later.

3 thoughts on “Will Tory plans to sell council houses to fund new affordable rented homes work?”

Really like the data based analysis. Can’t wait for the sequel to see what you think it means for new council housebuilding so I can work out teh impact on my block sales…

I also think that in addition to the headwinds of high house prices and uncertainty over the economy and the future direction of house prices, there will still be the additional headwind of mortgage availability. If the discounts offered are 50% as you suggest, buyers may not need a large deposit, but they still need to find a lender willing to lend and there aren’t many of those around….

Really like the data based analysis. Can’t wait for the sequel to see what you think it means for new council housebuilding so I can work out teh impact on my block sales…

I also think that in addition to the headwinds of high house prices and uncertainty over the economy and the future direction of house prices, there will still be the additional headwind of mortgage availability. If the discounts offered are 50% as you suggest, buyers may not need a large deposit, but they still need to find a lender willing to lend and there aren’t many of those around….

I am currently renting from local council, and have been considering buying my property on the buy it now scheme, but the discount i was offered meant that if i bought it, i would struggle to afford the repayments, if the discount is at 50% i would not hesitate to buy, and be able to afford it. this would be the same for many people nation wide,. also help people get on the housing market. would the the 50% discount be available to all properties nation wide? or would it decrease for the lower price bracket homes?

Comments are closed.