Mid-sized construction firms are being hit hardest financially according to Experian

Experian has put together what looks like an interesting piece of research that seems to support the view that it is the mid-sized rather than the large or small construction firms that are suffering the most financially in this recession.

Basically it suggests that if you are a mid-sized construction company employing 51 to 100 people and based in the North East you’ve probably borne the brunt of the industry’s recession.

Before going into more detail, it’s probably worth providing a bit of a health warning.

Almost any research of this type on construction firms is likely to run into problems because however you slice and dice populations of construction firms you almost always end up with a rather mixed bag.

This research has split the data by the number of people employed, which is useful, but the types of firms within each band are likely to be very varied in terms of what work they do and where they sit in the industry structure.

So, for instance, in the mid-sized group we may well have a variety of larger specialist contractors mixed with smaller general contractors.

What is also not clear is what effect we may be experiencing within each band as a result of job shedding and company failures. Is there possibly survivor bias effects?

So before drawing too many hard and fast conclusions these are a couple of the questions you might want to have answered.

But bearing this in mind the research is interesting. It suggests that mid-sized firms are far more vulnerable than the national average. This corresponds with what many believe within the industry.

The story that Experian focuses on is the fact that while analysis of output data suggests that bigger firms are taking an increasing amount of the work available, it is the mid-sized firms rather than the smallest that are under most pressure.

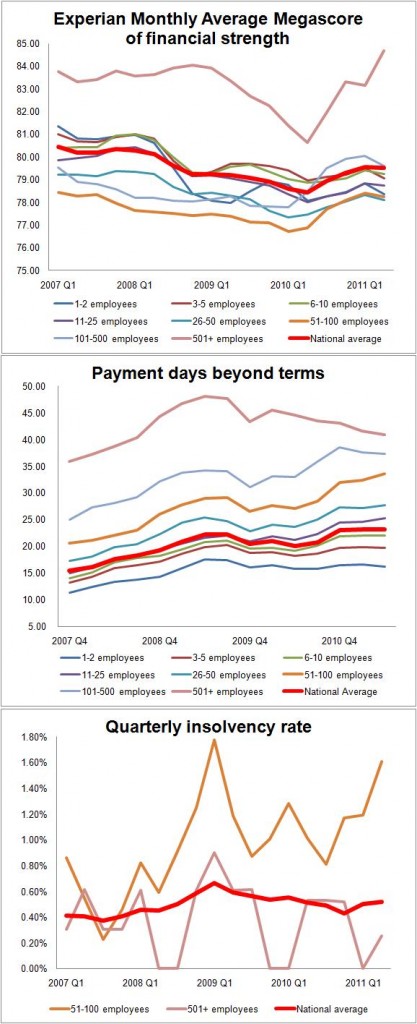

Experian applied its analysis of financial strength by what it calls its megascore which rates firms 0 to 100 – the higher the megascore the stronger the firms’ financial strength. It looked at insolvency rates as a percentage of the overall business population. And it analysed payment performance by the average number of days beyond terms that firms in each group pay their bills.

Each of these measures was looked at by size of firm. Experian also looked at insolvencies broken down by region.

Looking across the measures it used Experian’s analysis was that firms in the employee range 51-100 are having the toughest time during this recession.

On the graphs, I have altered them in format a little. I slightly highlighted the biggest firms (sort of pink colour) and the firms employing 51-100 people (orange) and for the insolvency graph left just those two groups showing along with the national average.

I haven’t included the regional graph. But it shows those in North East doing worst and the southern-based firms holding up better. Scotland is interesting as it seems to have been doing well early on in the recession, but things appear to have deteriorated recently.

One of the things the Experian analysis points to is the recent fairly sharp rise in the delayed payments from firms in the group with 51-100 employees. Fast rising delays in payment is one signal of potential financial stress. And as we can see the insolvency rate within this group has picked up in the past two quarters.

Experian explains the problems being experienced within this group by suggesting that bigger firms are taking on smaller contracts to bolster their turnover. This means less revenue for mid-sized firms.

However, mid-sized firms still have to maintain the same basic overheads. This means that they can’t compete easily with overhead-light smaller firms for small jobs but also can’t easily shed costs.

There were two other things that struck me when I looked at the graphs. First was how much improvement there appears to have been to the financial strength of the big firms in the past three quarters.

This seems clearly connected with the surge in work we experienced last year as a result of the fiscal stimulus and restocking among house builders.

Clearly having financially stronger firms is encouraging, the question however is whether this is a passing phase.

But what was more disturbing was the decline in the financial strength of all other firms in the second quarter of this year.

I don’t know, but I suspect that the financial strength scoring is a lag indicator and I also suspect that firms employing fewer people are more sensitive to changes in the market, so this drop may well be pointing to either a slowdown in construction work or a financial squeeze from falling prices and rising costs or possibly both.

Whatever the full meaning of the survey, it does provide food for thought and, in these troubled times, more reasons to be cautious.