Markit/CIPS survey suggests solid growth in construction in July, was growth that solid?

The latest Markit/CIPS PMI construction survey provides on the face of it reasons to be content if not cheerful in these days when gloomy news is served so liberally.

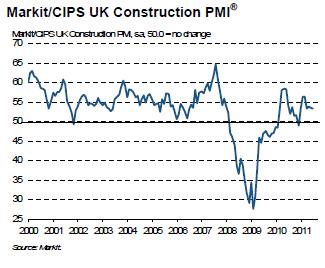

Its monthly PMI indicator for July read 53.5 against 53.6 in June. This suggests sound if not spectacular growth (see the graph taken from the press release (pdf)), which seems rather at odds with the more downbeat noises coming from across the industry.

But dig a bit deeper into the figures and things are not that comforting, especially if we look at this index in its historical context.

But dig a bit deeper into the figures and things are not that comforting, especially if we look at this index in its historical context.

We see that it is civil engineering helped to pump up the volume in the index in July following its growth in June. Meanwhile there was growth in the commercial sector, but it slackened in July having held up the index in June. Growth in the housing sector on the other hand remained negative for the second month in a row.

I must confess to some ignorance (and slackness for not inquiring beyond reading the notes to editors) on how precisely the index weights these sectors, how it relates its sampling frame to the population as a whole, how it takes account of seasonal variations and what it includes and excludes.

But, with a sample of purchasing executives from 170 construction companies, it seems likely that a fair slice of what most of us think of as construction probably falls outside of the survey’s scope – small repairs and maintenance for instance.

So there is plenty of scope for this survey to be at variance with the official data and other trade surveys. And certainly its reported level of future work does tend to be much more positive than other surveys or indeed reality would suggest.

Indeed the July survey once again points to UK construction companies being optimistic that output will rise, although it points out that the optimism is not that strong if we look at historic data.

Meanwhile, the survey does pick up on some unsettling trends such as cuts in jobs and cuts in the use of subcontractors. It also again picks up on rising costs, pointing to fuel and copper prices in particular.

These index results do not provide sufficient evidence to convince me that output in the industry is actually expanding solidly and I’ll be interested to see what the latest official output figures, due out next week, have to say about growth in June.