Few signs in construction output figures of private sector revival. But who really knows?

Only a fool would try to make sense out of the latest set of ONS construction output figures.

So here goes.

Mind you I intend to glide gingerly over those bits where angels would fear to tread.

Now to the bald figures.

These show a month-on-month drop in construction work done in April of just under 14%. The bigger hit was to repair and maintenance work, 18% compared with a 12% drop in new work.

That looks pretty scary.

But let’s shoo away some of the fears such a drop might engender.

Compared with April last year the drop is less dramatic 2% drop. So pretty much the same given the vagaries of measuring construction work.

And remember, this was no ordinary April. This was Royal Wedding April and with Easter just a few days before inevitability plenty of people took the days off in between.

What impact that will have had on construction workflow who knows? But there was probably some additional slowdown.

Also the March figure from which the industry took this near 14% monthly fall was a bit perky, as you would expect in the run up to the end of the financial year and in a month when work tends to get done without too many God-sent or calendar interruptions.

The March figures clearly show a bit of liveliness in the public sector work and so, as one might expect, the fall of public work in April was more pronounced than work in the private sector.

Meanwhile, we have the confusing effect of the heavy snow in December, which held back progress on many a project. So we would expect to see a drop in that month and an exaggerated bounce back as firms sought to catch up on their schedules over the following months.

Meanwhile, we have the confusing effect of the heavy snow in December, which held back progress on many a project. So we would expect to see a drop in that month and an exaggerated bounce back as firms sought to catch up on their schedules over the following months.

But it’s hard to quantify just how much of a bounce there might have been and how far this (supposed) effect would spread.

Then from the confusion of what has been happening in the real world over recent months, we must look to the data itself.

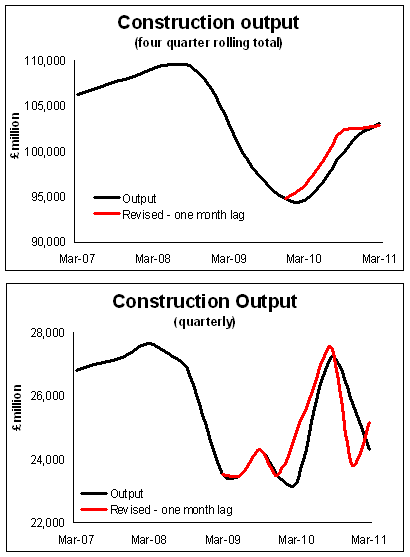

There is afoot a theory that the construction output data may lag the real world, which would suggest that the March figure might say more about February and the February figure about January and so on.

If there is juice in this notion we need to be a careful how we interpret the monthly changes in output.

For those who like to think visually I have done my best to chart what would happen to the shape of construction output if we pushed back the recent figures by a month. In reality there is unlikely to be an even lag in the various data, but what the heck see what you think.

Not really sure this improves the look of the curves that much in relation to what the mood is on the ground. But the quarterly revision does show a steeper drop in the final quarter of last year (which might have been expected given the heavy downfalls of snow) and a bounce back in the first quarter of this year, which would seem to fit better with the word on the street.

Meanwhile, having seen the graphs, to those who wonder how come the bounce back was so high in the middle months of last year I can offer no explanation other than it was probably (in part at least) down to the fiscal stimulus.

And, yes I agree, the suggestion that workload in 2010 Q3, when the industry had 210,000 fewer (10%) in the workforce, was more than the workload in 2007 Q3 is hard to swallow.

But let’s just say there are a few oddities in the figures, as they currently are structured, bear it in mind and move on.

So for all this confusion in the numbers, what are they really saying?

For this I think you really have to take account of, at least in the back of your mind, the pipeline and other survey data.

But the general impression the figures give, taking all the above factors into account and trying to look through the exceptional bumps and dips, is that the underlying trend is one of an industry sliding back into recession.

The falling away of public sector work seems clear in the figures. But what’s disturbing is that the private sector is not performing with enough vigour to provide confidence that it will much dampen the decline.

For all the excitement about the shiny new towers being erected in London, the data on office building suggests decline and the same is true of retail. Meanwhile, the private housing figures provide little comfort.

On the plus-ish side is infrastructure where output is relatively buoyant, but the new orders figures suggest that might be fairly short lived.

So the conclusion one is left with is not good and much the same as when we looked at the new orders figures.

The industry looks as if it will be dragged down with the decent of public spending while the private sector limps along offering limited support, more in some parts of the country than in others.