How worrying is the latest jump in inflation?

The latest jump in CPI inflation is worrying – at least to me.

Yes Mervyn King, the Governor of the Bank of England, had sought to soften views by warning with the release of the latest Inflation Report that there may be spikes ahead.

And economist had been expecting a rise this month – although not this big.

But looking at the hard figures, the jump of more than 1.1% in a month – a fairly rare event – seems to me to be quite disturbing in itself.

However, more disturbingly we are seeing the acceleration in inflation in what is described as core inflation (excluding things like energy, food, alcohol and tobacco) and also, more worrying still, in services.

Meanwhile, inflation in the pipeline also remains a concern, with producer prices remaining stubbornly high. Output price inflation (excluding excise duty) remained at 5.5% last month, having risen steadily over recent months.

Naturally there were freak events causing much of the rise in the latest CPI index, but there always will be some freak events given the size of the basket of goods measured.

This month it was a weird coincidence of the timing of Easter with the measurement of air and seas fares that in large part influenced the annual jump, along with a bump up in the price of fags and booze.

No doubt, also, the Bank of England is looking for some of the recent rise in headline inflation that is down to the feed-through of tax increases to fade and drop out of the index in due course.

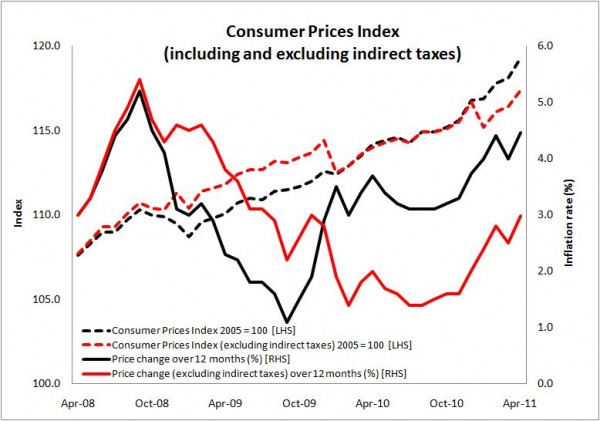

Even so, once the effects of taxation are taken into account the picture still is one of high and rising inflation, as graph 1 (above) shows.

The Bank will also be hoping that the feeding through of rises in commodity prices will also be a temporary factor.

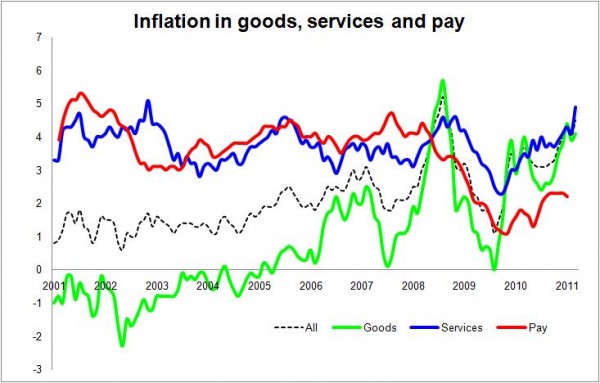

For my money, however, that the rate of CPI services inflation has been rising and is now at 4.9% – its highest rate since 1993 barring one freak peak in December 2002 – should be taken particularly seriously, as a far larger element of this is home grown inflation, rather than imported.

As graph 2 shows there is a fairly strong relationship between services inflation and pay inflation. This leaves a nagging worry over the potential that may be opening up for upward pressure on wages leading to a further rise in services inflation – an upward spiral.

No doubt the Bank will be hopeful that the severe fiscal tightening and the rate of unemployment will help to constrain upward wage pressures with firms eager to remain cost competitive in a tough market. That would be good news for inflation, but not so good news (at least in the short term) for those hard-pressed workers who have seen their earnings savaged of late.

Still the jump in inflation – while it unsettles me – didn’t seem to spook the markets and house building shares were not badly knocked by fear of a more imminent interest rate rise.

So perhaps my fears are overstated. The mood among most economists quoted in the press is that the rise is temporary.

But let’s face it, as a breed the economists quoted in the media have been woefully wrong about inflation up to now.

And I can’t help but be a shade more unsettled by inflation, as I have been over the past couple of years.

The last thing construction needs is for policy makers to be forced into an ugly battle with inflation.