Inflation rate will fall next month, probably, but it needs to fall sharply

The first look at the inflation figures provide plenty of room to be very pessimistic if you owe lots of money and are on a tight budget.

The jump in the CPI measure of inflation to 4.4% in February was more than many forecasters had expected. It will inevitably add to pressure on the Bank of England’s Monetary Policy Committee to raise interest rates – if for no other reason than a perceived need to restore its dented confidence.

For the housing market this will be a testing time as we will most likely see a noticeable lift in mortgages rates for new business for the first rise in more than a couple of years.

This might test just how fragile the housing market really is to mortgage increases.

But for all the perceived need to restore confidence, the Bank of England’s Governor Mervyn King is most likely right when he says inflation will fall. Indeed the headline inflation rate will fall next month if we don’t have the biggest spike seen more than 20 years in prices between February and March.

The most likely figure for headline CPI inflation next month based on February to March rises in the recent past is about 4.1%. So if we see inflation drop to 4.2% this will be no cause for celebration – it will just be the much-talked-of base effects.

But what no doubt is worrying the rate setters, more then many other things, is the way in which inflation may be entering the psyche of the nation. Inflation expectations are rising according to the Bank of England’s survey and certainly the rate setters would not like to see the current level of inflation expectation become embedded.

We might well expect inflation in goods to be fairly volatile and to be high at present, with rises in international prices of commodities. And there is a limit to the control the Bank of England can have over rising prices of imported goods, other than, perhaps, through raising interest rates to lift the exchange rate of the pound.

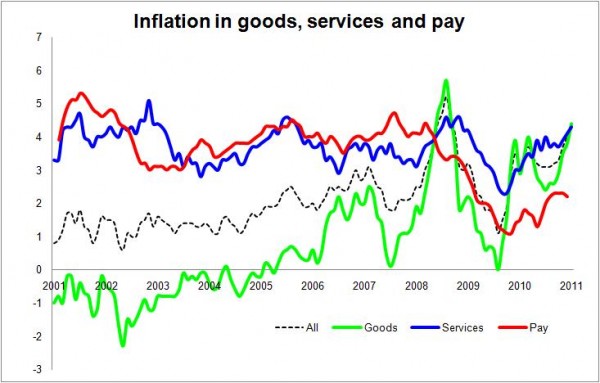

The graph shows CPI goods and services inflation rates (%), and the overall CPI headline rate of inflation. The pay data is for the three-month average year-on-year growth seasonally adjusted for regular pay within the whole economy taken from the Average Weekly Earnings dataset.

The graph shows CPI goods and services inflation rates (%), and the overall CPI headline rate of inflation. The pay data is for the three-month average year-on-year growth seasonally adjusted for regular pay within the whole economy taken from the Average Weekly Earnings dataset.

The focus will perhaps be more on services inflation, which interestingly and unsettling is rising again and fairly strongly – reaching 4.3% in February. Some of this rise will be down to the rise in VAT and imported commodity costs feeding through.

But, as we see from the graph above, inflation in services does appear to be much more stable. This suggests that pulling down this element of inflation – which accounts for about 44% of the total – might prove tough. And, given that it is strongly related to pay, it will almost inevitably prove painful, in that downward pressure on services inflation will suppress workers’ already squeezed wages.