Public sector job cuts and the housing market

There has been some rather unsettling data released over recent days for those who fear falling house prices.

The latest Bank of England data showed seasonally adjusted mortgage lending falling by 10% in December to a level not seen since May 2009 when the housing market slumped.

Nationwide’s house price index showed a further slight fall of 0.1% in January, which when other indicies are considered suggest prices are on a downward path.

Meanwhile there are worrying signs of falling consumer confidence following the introduction of a higher rate of VAT and announcements of a swathe of redundancies across the public sector. The GfK NOP consumer confidence index plunged in January to the lowest level since March 2009, with confidence in the economy continuing to slide rapidly.

Things are clearly not conducive to a buoyant housing market. But, with ultra-low mortgage rates, the market has so far managed to absorb much of what was thrown at it after the initial freefall in 2008.

It’s generally accepted that it was the drying up of mortgage finance in the wake of the credit crunch in September 2007 that precipitated the sharp fall in house prices that accelerated through 2008.

On the surface the market appears to have absorbed the sharp rise in unemployment from about 6% of the economically active to about 8% within the space of a year following the Lehman Brothers collapse which is credited with firing the starting pistol on the recession.

This naturally provides some confidence as the nation prepares to accept large numbers of public servants onto the dole queues with the savage cuts being made to state spending.

But will it be different this time as the dole queues extend?

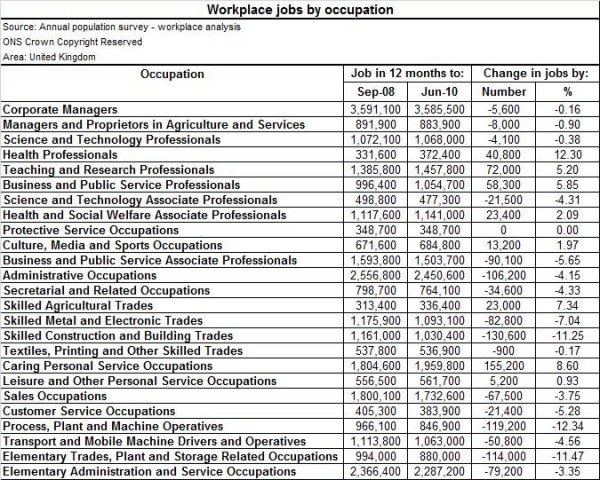

Firstly let’s consider what happened to employment over the period since the collapse of Lehman Brothers.

Comparing data from the nomis database (see above) for workforce jobs in the year to September 2008 with the year to June 2010, it would seem that the number of jobs among many of the better paid occupations has broadly risen. Certainly the jobs cull clearly hit, both proportionately and in sheer numbers, the less well paid hardest.

This suggests that where homeownership is more prevalent – among the better off – there has probably been a net gain in jobs, with job losses concentrated more among those that are more likely to rent.

This is rough and ready stuff, but it does provide some insight into why rising unemployment appears not to have had that big an effect on the housing market. Clearly there has been distress in some quarters and repossessions have risen, but perhaps not as much as the headline unemployment figures might have lead one to imagine.

Now let’s consider what might happen with cuts to the public sector.

Much is made of the fact that the public sector average wage has been rising faster than that in the private sector for many years and that on average public servants earn more than those in the private sector.

It would be simple – and lazy thinking – to dismiss this as the result of cosy pay deals. Although it is true that the public sector would have been more sheltered to date from the cuts in pay or hours of the scale suffered by many in the private sector.

But it must be remembered that there is both confusion and fun to be had when using and abusing averages. Recall the quip by former New Zealand Prime Minister Rob Muldoon when quizzed on New Zealanders moving to Australia. He suggested it was of mutual benefit as it led to a rise in the average IQ in both nations.

We have to be considered when we look at public sector average earnings. The outsourcing which has taken place over recent years has tended to traffic lower paid jobs into the private sector. This alone would raise the average earnings within the public sector and reduce it in the private sector without change to the particular pay of those who remain.

We must also be aware of any confusion caused by the absorption of a large part of banking into the public sector count.

But the critical point here is that the public sector has become more densely populated with better paid occupations than the private sector.

From that it seems reasonable to assume that employees within the public sector are likely to be more densely represented within the homeowning class. (If anyone has figures on that please let me know)

It also seems reasonable to assume, then, that when the cuts bite the within the public sector we will see a large swathe of relatively well-paid employees lose their jobs rather than simply the loss of lower paid jobs.

Indeed as the public sector has to pick up the tab for the social cost of unemployment it makes sense to cut better paid jobs than lower paid jobs if the nation is after a net saving.

Anyway the natural corollary would appear to be that the coming wave of job losses might well be significantly more impactful on the housing market than the first wave.

How impactful is anyone’s guess. But it will certainly be more testing.