Nationwide joins other indexes to show house prices falling

It came as little surprise that the Nationwide house price survey should show a fall in July. And it showed a pretty significant fall of 0.5% on its seasonally adjusted series.

It had been for many months among the more bullish of the indexes measuring inflation in the UK housing market, at a time when others were showing the market sliding backwards.

But like most of the indexes, the Nationwide has had to draw big conclusions from a rather thinner pool of data, with transactions historically low. And there is good reason to suppose that that people and houses trading in the market are not as representative as one might like of those who trade in a more normal market.

So it is wise to be more cautious than normal about drawing too close a relationship between house price indexes and the real value of housing.

Still, health warnings aside, this release adds weight to the growing view that the housing market is cooling and prices are set to stagnate if not slip back in the coming months.

And there was further evidence today to suggest house prices might slip further from the Bank of England statistics that showed mortgage approvals down again in June.

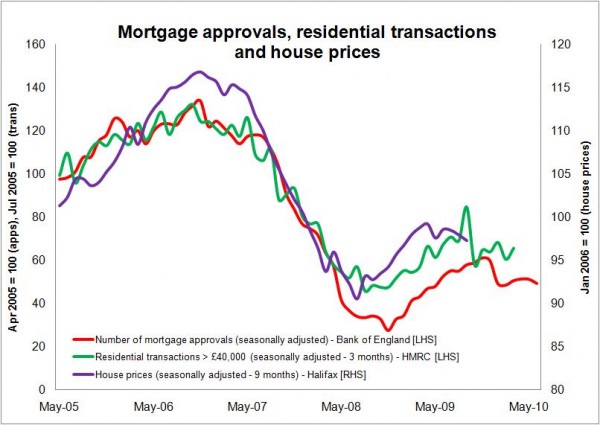

I have once again updated my pet graph showing the Halifax index against transaction and mortgage approvals with various lags. I am not sure that the lags hold that firmly, but the line of house prices as measured by Halifax does seem to be behaving broadly as expected when I first put together this particular graph in March.

I have once again updated my pet graph showing the Halifax index against transaction and mortgage approvals with various lags. I am not sure that the lags hold that firmly, but the line of house prices as measured by Halifax does seem to be behaving broadly as expected when I first put together this particular graph in March.

Anyway, the question I guess most concerning most people is: How far and fast might prices slip?

The Economist magazine regularly publishes a ranking of global house prices and rates them on whether they are over or undervalued.

Most are overvalued, not surprisingly given the recent global boom. But there are notable exceptions in Japan and Germany which saw years of house price deflation.

On the Economist’s scale, house prices in Britain are 33.8% overvalued when last looked at. This is broadly in line with the view of many commentators.

There will be those that argue this is an immediate cause for concern and reason to fear a second severe slump in UK house prices. It would be ill advised to simply dismiss this out of hand.

But the consensus view from the comments I read and chats I have with those I respect most on these matters points to a slide back in nominal house prices. But they don’t foresee a collapse on the scale of that seen in 2008.

The view seem to be that, without a trigger such as rapidly rising unemployment or a sharp hike in interest rates, there will be a flat slightly downward trend in nominal house prices and inflation will eat more deeply into the real value.

This seems a pretty sensible take. And I note it is broadly in line with the view expressed in the report out this week by the think tank NIESR. It expects house prices to slide by 8% in real terms by 2015. With inflation above 2% that drop only requires nominal house prices to stand still or slide a fraction for two to three years.

The main support for this view, and that house prices will not collapse in nominal terms, is that interest rates will stay super low for an extended period. NIESR reckons mortgage rates will stay below 5% for most of the next three years.

Meanwhile, the economic forecasting group the Item Club reckons suggests rates will stay lower for longer. It has penned into its forecast a three-month interest rate of 0.7% in 2013 and 1.2% in 2014, a percentage point or more lower than the NIESR forecast for 2014.

And the noises coming from the man who probably has more say than most in these matters, the Bank of England Govenor Mervyn King, seems to support the view that interest rates may well be low for a long time yet.

He told the House of Commons’ Treasury Committee this week that: “It’s right to keep our foot firmly on the monetary accelerator.”

By this he means keeping interest rates low and, we shall see, possibly pumping more liquidity into the economy through quantitative easing if it proves necessary.

But he was very clear about the difficulty of the choices facing the Bank’s Monetary Policy Committee, saying that there was a danger high inflation might become ingrained in inflation expectations. And, he said, it would then be hard to bring inflation back down again.

So if the MPC’s preferred choice now to take the low interest rate road proves the wrong one and we end up with unacceptably high inflation we should perhaps expect to see the committee hiking rapidly uphill to the high interest rate road in more of a hurry than would be comfortable for those exposed to debt.

All of a bit of a worry whether you are in the “keep house prices rising” or the “let ‘em plunge” camp.

But as things stand, on the basis of what we can see, it would seem fair to say that a collapse in prices of the scale we saw in 2008 is unlikely, but a readjustment is on the cards. Although, with the economy delicately balanced, the circumstances that might lead you to that view could change and change pretty quickly.

There is one further point worth considering for those in construction. What are the consequences if there is no downward adjustment in the ‘real’ price of houses in the UK?

When interest rates rise, as they will, the barriers to entry for new buyers will rise sharply. If prices then remain high, the chances of choking off still further the already limited demand from first-time buyers is evident. The result would most likely be a greatly suppressed level of transactions.

This ultimately represents a nasty threat to the UK house building industry which, recent history suggests, relies on liquidity in the housing market. When transactions overall are low sales of new homes are also low.

Still, I suspect we will have a few more twists in the house-price saga in the coming months and years before we get a more settled pattern resembling steady sustainable growth.