Joy deferred as CIPS shows construction activity grows for first time in two years

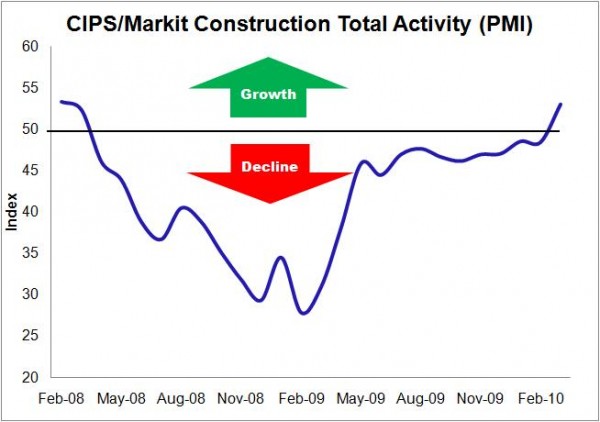

So the construction activity indicator produced by the buyers’ body CIPS finally points to growth after two years of measuring falling workloads. But this seemingly uplifting moment appears to have brought little joy.

The March figure popped its head above the 50 no-change mark on the back of rising activity in the housing and commercial sectors. But the survey also found more and deeper job cuts within the industry and there was a drop in the confidence within firms over future levels of work.

The March figure popped its head above the 50 no-change mark on the back of rising activity in the housing and commercial sectors. But the survey also found more and deeper job cuts within the industry and there was a drop in the confidence within firms over future levels of work.

Firstly it must be remembered that this figure could prove to be a statistical anomaly. A point that wasn’t mentioned with the release accompanying the data, but should have been, is the impact of a bounce back in activity from the cold snap earlier in the year. Some if not all of the rise in March could be down to firms playing catch up.

But, even setting that observation aside, the apparently contradictory findings of more work accompanied by cuts in employment will come as little surprise to most industry watchers.

The huge sums of public money propping the industry have helped to ease the pain as work in the private sector fell.

From a very low base private sector activity may be patchily rising – hence it would be no surprise to see a rise in workload.

But from here the props provided by the public sector will gradually be dismantled and most bosses within the industry fear that there might prove to be insufficient life within the private sector to make up for the shortfall this will mean in workload.

We are at a pretty critical stage as things stand and the hot money is on a double-dip recession in construction.

Worse still, as firms struggle to deal with low rising or even falling workloads from here they will have yet another problem to deal with.

The CIPS survey noted rising input costs for the fifth month out of the past six. This is to be and should have been expected.

The commodity price falls we saw in the wake of the credit crunch are now reversing.

Steel prices, which have captured recent headlines with the introduction of a new pricing deal, have roughly doubled over the past year from the deep low reached in early 2009. We have seen oil and copper prices also double over the period. All however remain below their pre-credit-crunch levels.

These falls had disguised the inflationary effect on imported materials of the falling value of the pound which is now trading about a quarter lower than pre-credit-crunch levels on a trade weighted basis.

From now on firms should start to expect prices to rise fairly strongly.

And, although less of a threat, rising commodity prices also should concern construction firms from a broader economic perspective, if the rises end up contributing significantly to inflationary pressures within the UK and in turn force an earlier rise in interest rates. This would inhibit growth in both the housing and commercial sectors which are central to the recovery in construction.