How quickly can the Government cut back on construction spending?

It was put to me recently that, despite all talk of cuts to capital spending, many contractors held the view that UK governments have never managed to make cuts of more than 10% year on year.

I wasn’t quite sure what to make of this, but three things struck me.

Firstly: I wasn’t clear on what might have been meant by “capital spending” and whether the contractors may have meant just public sector capital spending on construction or overall government capital spending.

Secondly: the 10% figure surely was wrong, so I needed to check it.

And thirdly: I wouldn’t be blasé about a 10% year-on-year cut, particularly if it continued over a few years.

Nevertheless, the comment prompted me give some thought to just how quickly the axe might fall on public funded construction.

The obvious first place to look to get a historical perspective is the early days under Margaret Thatcher. And true enough the cuts in the period 1979 to 1982 were more savage that 10% per annum.

If we examine public sector net investment (the capital budget line) we see it was shredded in the early years of the Thatcher administration and public sector gross investment (a broader measure that includes a sum for depreciation) fell by 14.3% in real terms in the financial year 1981-2.

That is about the scale projected within the Pre-Budget Report for PSGI in 2010-11 once you factor in an estimate for inflation.

Looking at construction (new work only) from crude calculations it appears that a couple of the annual drops in public sector funded work (at constant prices) during that period were between 12% and 15%.

What was, however, more significant about the Thatcher years was the persistent cutting in spending.

Overall the sector appears to have declined by 40% or so over a four or five year period.

But you don’t have to look back to Ms Thatcher’s axe wielding powers to see examples of severity on the Treasury chopping block.

I have put together a couple of graphs of public sector gross fixed capital formation (GFCF), from the period 1986 to more or less the present, showing both the annual changes and the level of government capital investment.

I have put together a couple of graphs of public sector gross fixed capital formation (GFCF), from the period 1986 to more or less the present, showing both the annual changes and the level of government capital investment.

The first of these graphs shows overall public sector GFCF, the second takes only the lines for GFCF “dwellings, buildings and structures”. The reason for using this measure is that the lines for GFCF “dwellings, buildings and structures” when totted up for private, public non-financial corporations and general government closely match total construction output.

There is a health warning here, the effects of privatisation and PFI/PPP do cloud the figures in ways that I dare not even try to explain.

What I have done it to rebase the numbers to 2008 prices using the Treasury GDP deflators to adjust the money spent in a way that accounts for inflation.

Anyway what we see are some pretty severe drops, although part of this can be assumed to be related to privatisation.

So, the idea that there have not been cuts in government capital spending of greater than 10% seems to be at the very least questionable.

It would seem from history that, if the government of the day has a will and is sufficiently eager and pressed enough, it can cut faster than 10% year on year and for a number of years.

And if the cuts are sustained for three, four or even five years (though with the electoral cycle being as it is five years is unlikely), the pain could be immense.

What is clear is that the next incoming government will have more reason than most to axe public spending. It is an imperative that the nation firstly slows its borrowing and then reduces its debt.

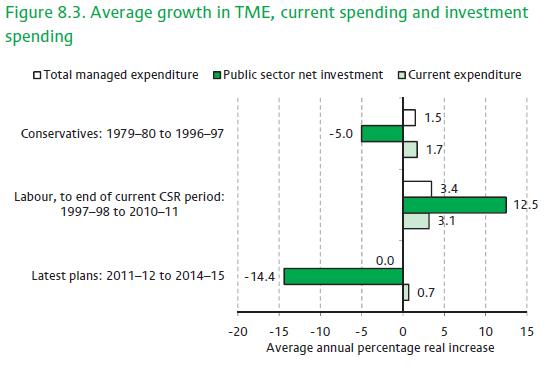

The Pre-Budget Report does provide indications of the scale of capital spending cuts planned. They are pretty savage in historic terms, as is seen by the projections for public sector net and gross investment (see graph).

The Pre-Budget Report does provide indications of the scale of capital spending cuts planned. They are pretty savage in historic terms, as is seen by the projections for public sector net and gross investment (see graph).

But what is more worrying is that these cuts are premised on an expansion in the economy that many, nay most, economists find optimistic or “wildly optimistic”.

The recent published IFS Green Budget, by the well respected Institute of Fiscal Studies, puts as its central case growth in the four years 2011-12 and onward at between one and two per cent below the PBR figures. It does, however, see a slightly stronger immediate bounce out of recession, so the base is slightly higher.

The Treasury case is that it will use strong growth to generate the funds to pay off the debt. If the growth is not so forthcoming, as many suspect, an alternative will be needed and the most readily available is more savage cuts.

I have included a graph from IFS which puts into context the scale of cuts planned in the Pre-Budget report.

I have included a graph from IFS which puts into context the scale of cuts planned in the Pre-Budget report.

What is more as IFS points out, the Government has pledged to protect health, schools and overseas aid, which limits the scope for cuts and means the burden falls disproportionately heavily on those unprotected areas of spending.

Further another bind that the Government faces is that for each cut it makes in public sector spending there will be associated job losses. So any savings made are only partial as, in the short term at least, the claimant count and public spending on welfare rise while simultaneously the tax take falls. That is to say the savings, particularly when they fall on low paid jobs, can be pretty marginal unless the private sector is able to employ those made redundant fairly rapidly.

This will weigh on the minds of government strategists, who may well go for the tried and tested route of cutting deeper into investment spending where the benefits are seen less immediately.

However the next few years do eventually pan out, one thing is certain: there is little scope for a complacent attitude to potential public sector cuts.

Nobody knows the future, but when the axe does finally descend on construction, there is a more than an evens chance that it will be wielded with more brutality than has been seen this side of a world war.