Orders figures support view that there is cause for concern in construction

The main message in the construction new orders figures released by ONS this morning is that the slope is downward and this is points to further falls in output in the future.

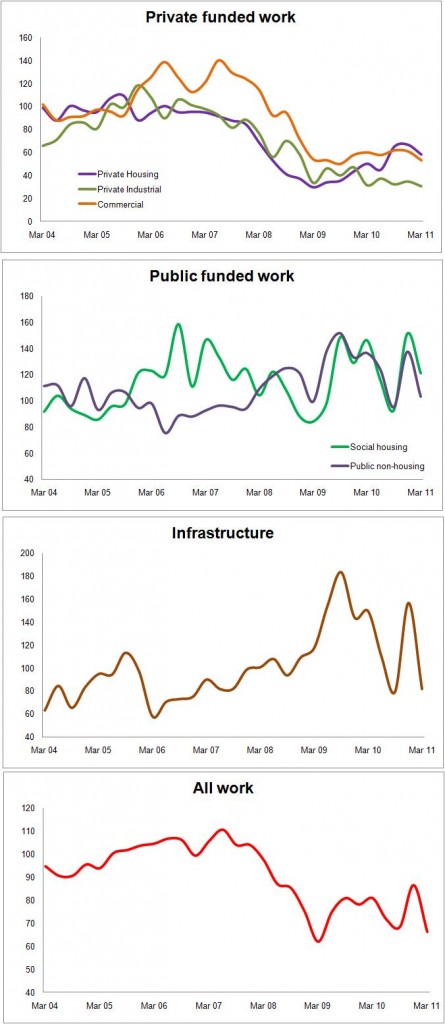

And, to put them in context, against peak levels in cash terms orders for new construction work are down about a third.

But more worryingly we don’t appear to be seeing the kind of acceleration in the private sector we would need to compensate for the losses faced in public sector work and pull the industry back into growth.

That said, the orders figures are extremely tricky to read at the moment, as there have been so many factors creating big waves in the underlying trends.

The bald figures suggest a drop of 23.4% quarter-on-quarter in seasonally adjusted volumes from the final quarter of 2010 to the first quarter of 2011. This follows a 26.3% rise in the previous quarter.

Neither figure should not be taken blankly without consideration of the context.

The drop this time is a drop from a mini-peak caused by the surge in work let in the final quarter of last year, which in turn was almost certainly a rebound caused by a hiatus in letting work around and after the General Election.

You need to smooth this all out and take a longer view to get a more meaningful picture of the underlying trend.

As I blogged when the previous set of figures were published showing a 18% rise (before the recent revision), the underlying picture was then a cause for concern. And the latest figures fit with that judgement – no more, no less.

But what this latest set of figures seem to add is more confirmation that there was a hiatus in letting work cause by the change of Government. It also adds further, if worrying, evidence that the response of the private sector is weak.

The figures also appear to support the least kept secret that the it’s grim up North for construction firms, with London the least badly hit and showing far more promise of growth.

Meanwhile, the response of the private housing sector is also intriguing. We might have expected a surge in work in the first quarter as developers geared up stock ready for the spring selling season. Well it didn’t happen, so it would seem that builders are becoming more cautious in their approach and choosing to build much more in line with actual rather than expected demand.

The graphs below give a flavour of where we are at. They show the index value for each main sector of new work orders.